As we kick off a new earnings season, we start again with Inter. The 800-pound Gorilla, who reigns supreme in the chip-making world, reports fourth-quarter 2022 and his full-year 2022 results, capping off what has been an increasingly difficult year for the company. As Intel’s key client and data center markets have reached saturation on the back of record sales and spending has slowed for the foreseeable future, Intel sees significant revenue declines in both markets. . These headwinds, not unexpectedly, broke Intel’s six-year streak of record annual revenues and put the company back in the red in the most recent quarter.

Starting with the quarterly results, for the fourth quarter of 2022, Intel reported revenue of $14 billion. This is a significant decrease of 32% over the same period last year. With Intel just dropping out of his year-old best Q4, as the saying goes, the higher the highs, the lower the lows. As a result, Q4 2022 will be on the books as a loss-making quarter (on a GAAP basis) for Intel, with the company losing his $661 million in the quarter and net income down his 114%. . Overall, Intel’s earnings for the quarter were already at the lower end of its conservative forecast range.

A quick comparison of the GAAP and non-GAAP numbers reveals a significant gap between the two, with official GAAP net income approximately $1.1 billion lower than baseline net income. So Intel was profitable at least on that core. jobs. To some extent, it looks like Intel is using what was already a bad quarter to record its GAAP expenses (such as restructuring and inventory write-downs), but at the end of the day, the company is particularly focused on R&D and other fixed costs. It has a fairly consistent cost overhead. cost. As such, a significant reduction in product sales will come from Intel’s bottom line. Ultimately, this reduced Intel’s quarterly gross margin to just 39.2%. This is below Intel’s breakeven point and well below the company’s historical standards.

The drop was driven by much of the same factor that has weighed on Intel’s earnings over the past six months. After a surge in product sales during the pandemic, the overall processor market reached saturation point and sales of both clients and servers declined. And with the prospect of a recession looming, business and consumer buyers alike are making their wallets more conservative. Not helped by some product release cycles, such as the just launched next-generation Sapphire Rapids server platform.

| Intel Q4 2022 Financial Results (GAAP) | ||||||

| Q4 2022 | Q3 2022 | Q4 2021 | year/year | |||

| Earnings | $14 billion | $15.3 billion | $20.5 billion | -32% | ||

| Operating income | -$1.1 billion | -$175 million | $5 billion | -one two three% | ||

| net income | -$661 million | billion dollars | $4.6 billion | -114% | ||

| gross profit | 39.2% | 42.6% | 53.6% | -14.5 points | ||

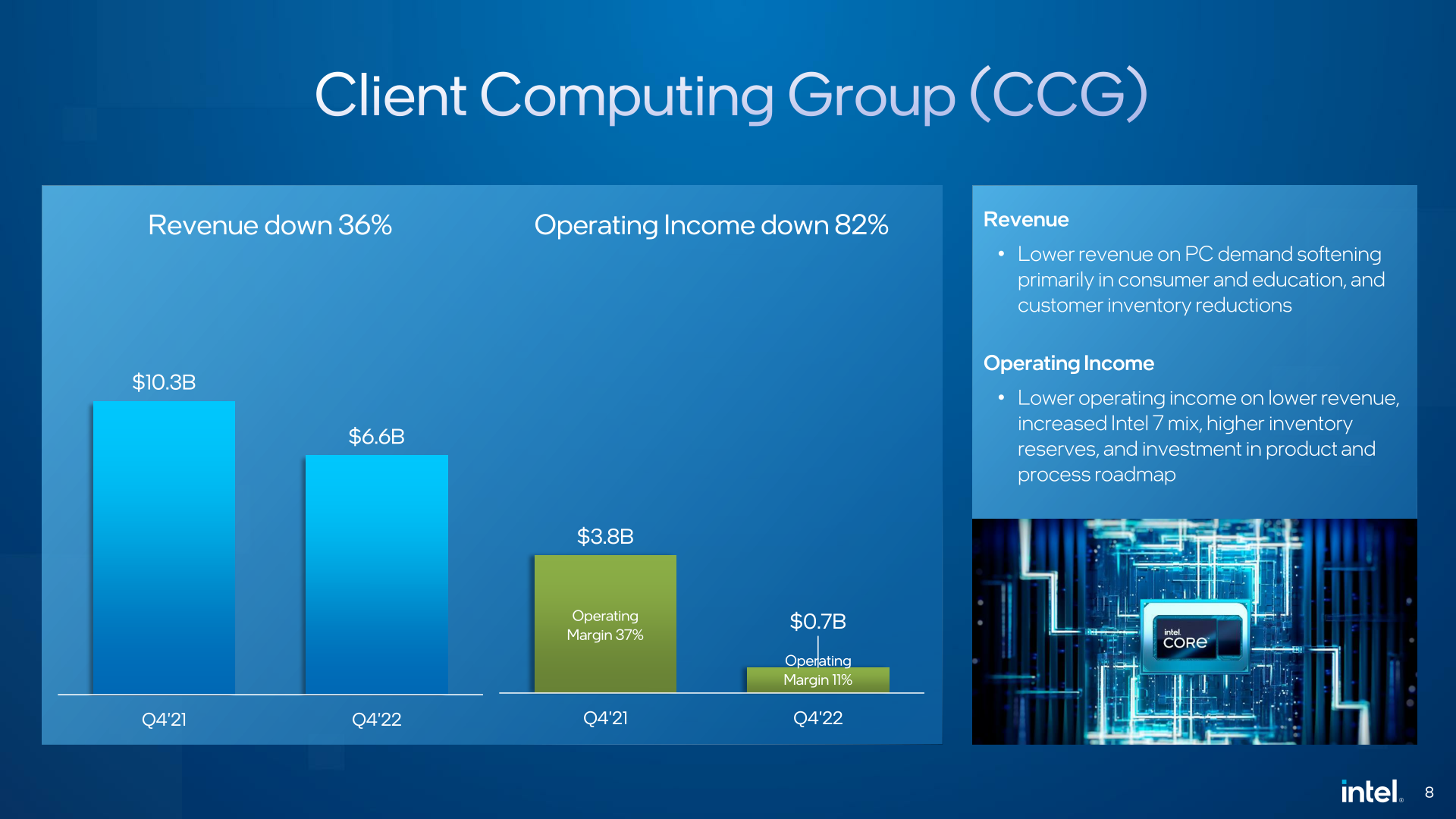

| client computing | $6.6 billion | $8.1 billion | $10.3 billion | -36% | ||

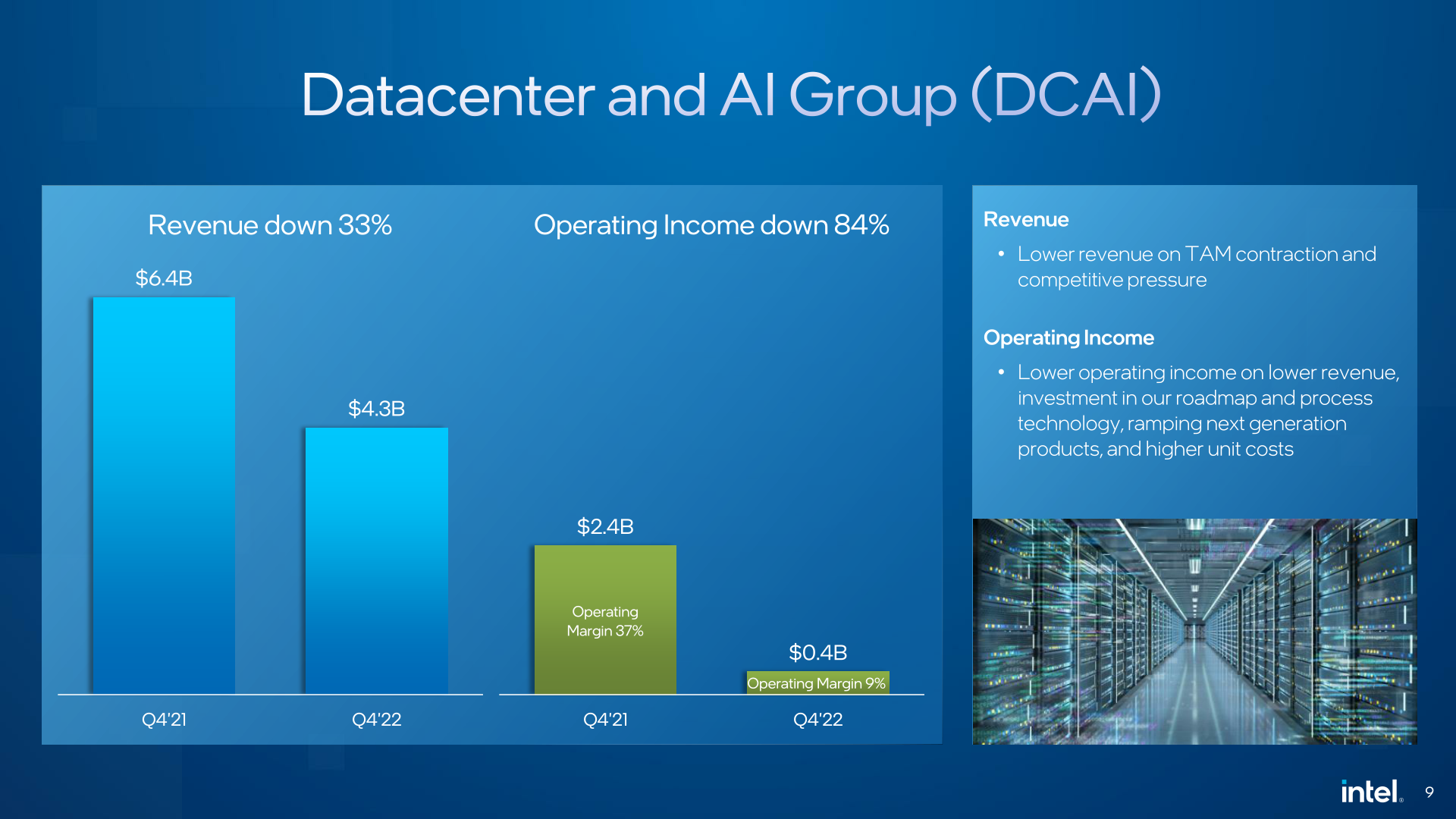

| Data Center & AI | $4.3 billion | $4.2 billion | $6.4 billion | -33% | ||

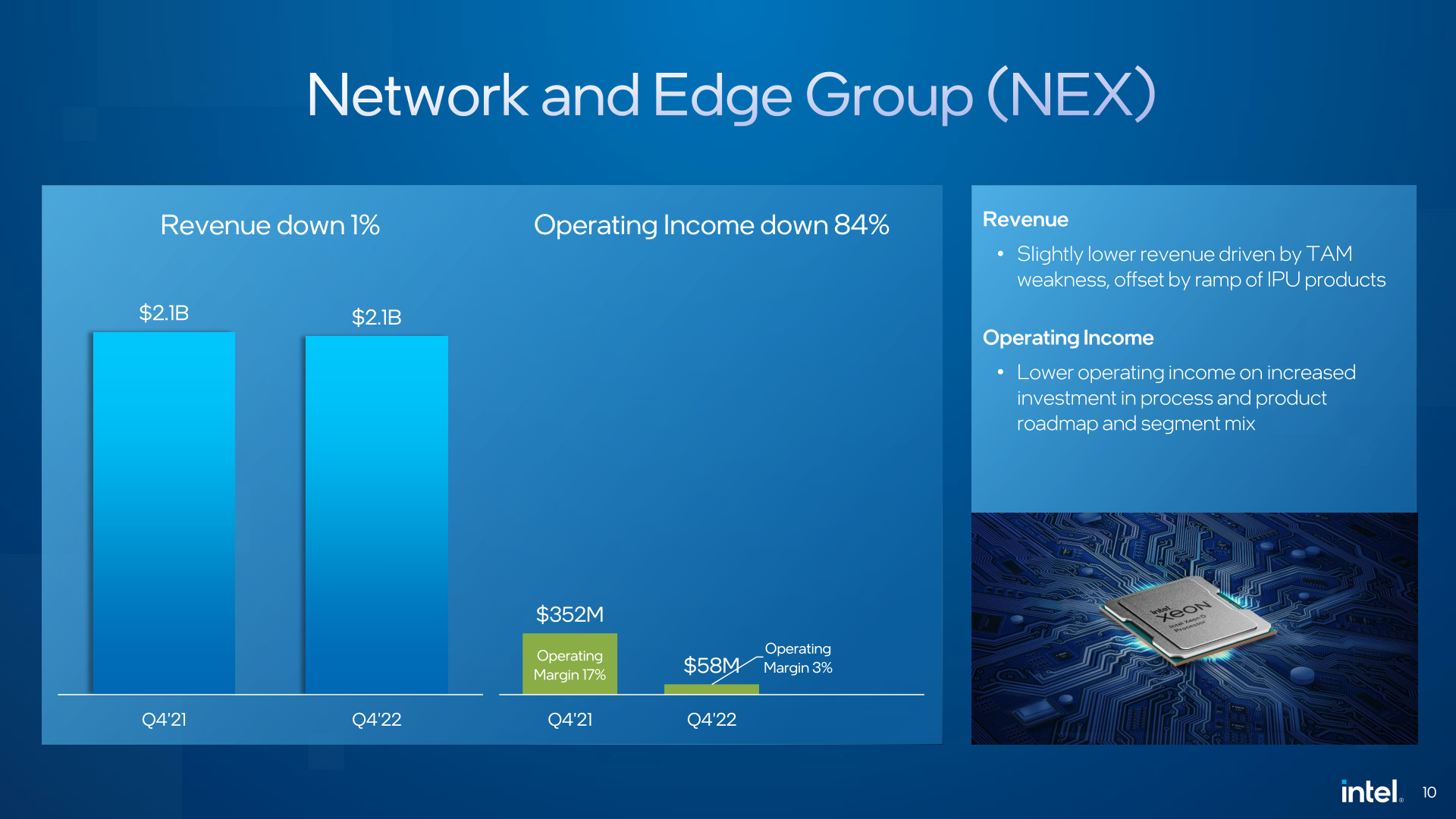

| network and edge | $2.1 billion | $2.3 billion | $2.1 billion | -1% | ||

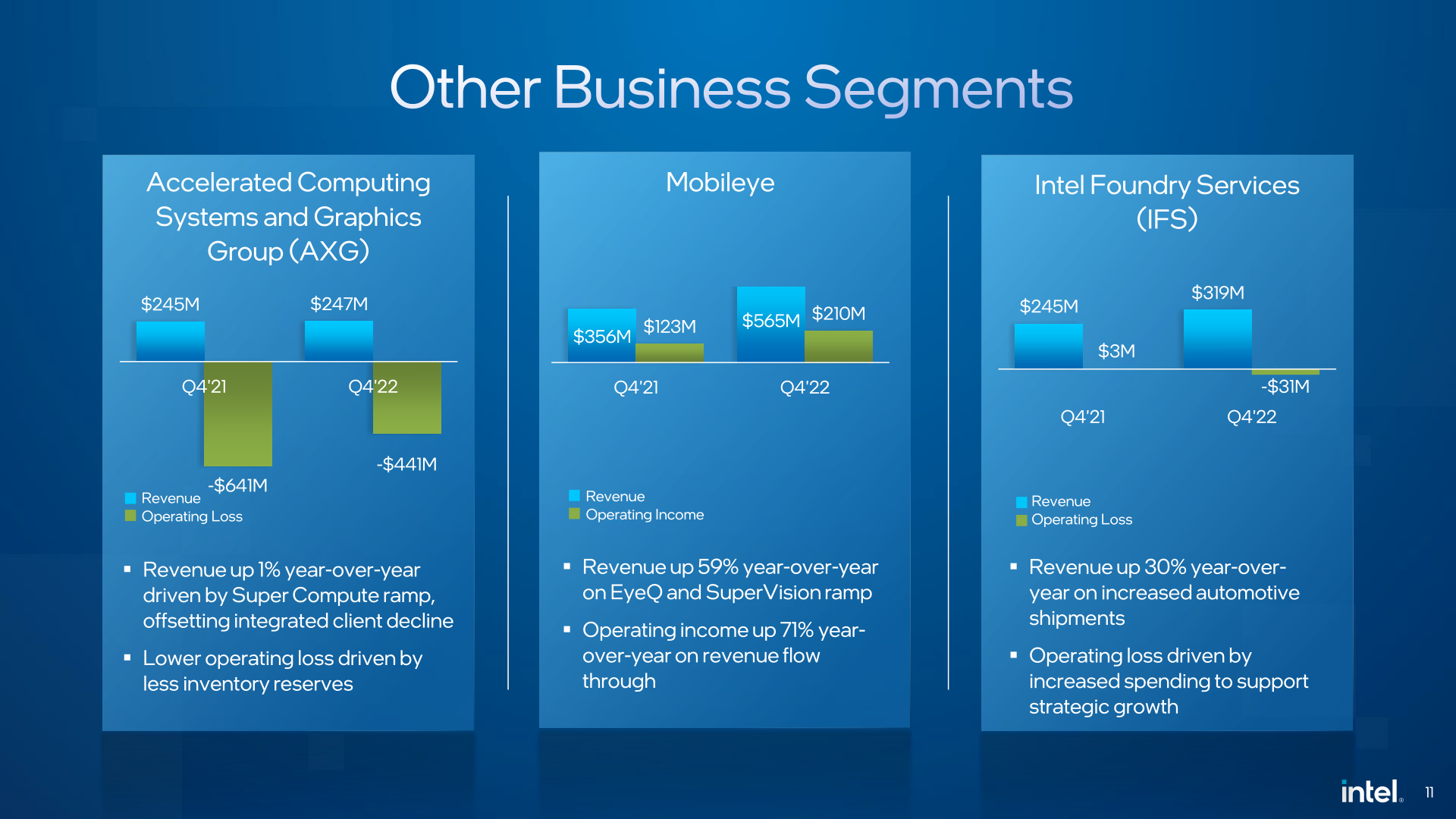

| Accelerated computing system and graphics | $247 million | $185 million | $245 million | +1% | ||

| mobile eye | $565 million | $450 million | $356 million | +59% | ||

| Intel Foundry Services | $319 million | $171 million | $245 million | +30% | ||

Broken down by group, Intel’s two core business groups, Client Computing (CCG) and Data Center (DCAI), both posted well below last year’s record highs. And in the case of CCG, revenue is down significantly from last quarter as well.

Intel’s customer group was barely profitable on an operating basis, despite a significant 36% drop in operating revenue. Considering this is Intel’s largest group by revenue, it’s a small win, but it’s actually a very small win since it only has about $700 million in operating profit. As I mentioned earlier, CCG has been bearing the brunt of the boom-bust cycle initiated by the pandemic, with end-user sales declining and Intel’s OEM customers running out of inventory they have. We are working to reduce the amount.

Digging into Intel’s sheet, client notebook revenue was $3.66 billion and client desktop revenue was $2.5 billion. Both were down more than 30% year-on-year, but notebook PC sales dropped significantly. This is a bit of a concern given Intel’s large percentage of client sales to begin with.Intel doesn’t disclose average selling price figures for the quarter, so how much of this decline is due to sales volumes and low prices. It is not clear what.

Meanwhile, data center and AI revenue fell 33% to $4.3 billion. This isn’t a steeper drop than the client group, but it’s slight. Unlike Intel’s client sales, DCAI faces challenges beyond industry-wide demand. Intel has been steadily losing server market share to rival his AMD, which launched its latest generation EPYC CPUs in Q4. On the other hand, Intel’s delayed next-generation Sapphire Rapids platform only launched a few weeks ago (Q5 2022), so even among Intel’s most loyal data center customers, there’s a lot of hype about Intel’s big server platforms. There was a pause as we waited for the update to finally become available. All the while Intel had to continue investing in Emerald Rapids and beyond.

Moving down the list, Intel’s Network and Edge group also finished the quarter year-over-year, but did much better overall and nearly broke even. Overall, the group posted revenue of $2.1 billion for him, down 1% from Q4 2021. However, operating profit is still significantly lower, which can be attributed to Intel’s investment in future products.

At least the silver lining for Intel in Q4 2022 is that all of the company’s smaller groups did well this quarter, with the exception of the big $1 billion+ revenue group. Accelerated Computing Systems and Graphics (AXG) revenue increased his 1% and operating loss narrowed. On the other hand, Mobileye and Intel Foundry Services both posted significant year-over-year growth. For Mobileye, the automotive group continues to expand its market and revenues, and Intel’s successful IPO of his Mobileye in the fourth quarter (which helped boost the value of their investment). Meanwhile, IFS continued to grow as Intel won new customer commitments and increased overall orders.

Full year 2023

Moving on to full-year results, 2022 served as a turning point for Intel’s earnings, which declined more slowly overall than in Q4 alone, but still made Q4 a very tough quarter for Intel. Overall revenue fell 20% to $63.1 billion, which led to a 60% drop in net income, notably Intel, which was still profitable on an annual basis and $8 billion.

| Intel 2022 Financial Results (GAAP) | ||||||

| 2022 | 2021 | 2020 | year/year | |||

| Earnings | $63.1 billion | $79 billion | $77.9 billion | -20% | ||

| Operating income | $2.3 billion | $19.5 billion | $23.7 billion | -88% | ||

| net income | $8 billion | $19.9 billion | $20.9 billion | -60% | ||

| gross profit | 42.6% | 55.4% | 56.0% | -12.8 points | ||

| client computing | $31.7 billion | $41.1 billion | none | -twenty three% | ||

| Data Center & AI | $19.2 billion | $22.7 billion | none | -15% | ||

| network and edge | $8.9 billion | $8 billion | none | +11% | ||

| Accelerated computing system and graphics | $837 million | $774 million | none | +8% | ||

| mobile eye | $1.9 billion | $1.4 billion | none | +35% | ||

| Intel Foundry Services | $895 million | $786 million | none | +14% | ||

Intel’s mix of good times and bad times is also reflected in Intel’s gross margin, which was 42.6% for the year. This is him down about 12.8 points from 2021, so 2022 wasn’t a great year for Inter. Meanwhile, as a minor balance sheet curiosity, Intel’s net profit this year was well above its meager $2.3 billion in operating profit. That gap is due to Intel’s investments and piles of cash generating good returns, with investments alone bringing the company’s annual GAAP net income to more than his $4 billion.

Since 2022 was the first year for Intel’s refactored business group, the company also provided a similar earnings comparison for 2021. , which is never good news. Client revenues were down 23% year-over-year, while data center revenues were down 15%. Otherwise, all of Intel’s remaining business units posted revenue growth this year. All but AXG have his double-digit growth.

Another major change on Intel’s balance sheet for fiscal 2022 and fiscal 2021 is Intel’s exit from the storage business. Selling the NAND business in 2021 was a net plus for Intel’s seat that year, but in 2022, it will write off its Optane memory products as the company looks to exit that business entirely. All in all, Intel received a total of $723 million in 2022 Optane inventory impairment charges. That includes his $164 million in the most recent quarter.

Expectations for 2022

We tend to pay less attention to Intel’s future earnings projections, but given the rough shape of the current processor market, it’s easy to see predictions for Q1 2023.

In short, Intel wants things to get worse before they get better. The company’s official forecast for Q1 2023 puts revenue at just over $10 billion, about 40% lower than his Q1 2022. As a result, Intel’s gross margin is expected to remain at 39%, with Intel forecasting the first quarter to be another loss-making quarter with his negative EPS. Intel’s slides use non-GAAP, but the projected GAAP number is even worse, at -$0.80 per share.

As we enter 2023, it will be the first year that Intel’s cost-cutting strategy, which the company first embarked on late last year, will take effect. Looking to cut costs without upsetting the company or affecting the development of Intel’s next-generation fab process, Intel is aiming to cut his $3 billion in costs by 2023.

Aside from these efforts, in another effort to reduce costs, Intel has revealed that it is extending the deprecation schedule for “certain production machinery and equipment” from five to eight years. In other words, Intel now expects this equipment to have a longer useful life than originally expected and/or planned. As a result, Intel expects he can save about $4.2 billion in depreciation in 2023. These changes have already been factored into Intel’s Q1 2023 earnings guidance, so even though Intel’s Q1 forecast looks grim now, technically things are going well. It can get even worse.

Finally, looking at Intel’s product and process roadmap for this year, there isn’t much new to report so far. Intel will continue to work on enhancing their Meteor Lake client SoCs later this year. This will be Intel’s first client product built on the Intel 4 process. This will be followed in 2024 by the new Lunar Lake platform. Recently completed the first tape out of his one of the tiles.

On the server side, Intel is looking to make up for lost time now that Sapphire Rapids has launched. The official server schedule is for Emerald Rapids to launch later this year, delivering a modest update to Intel’s Rapids platform. Emerald Rapids, like his Sapphire, is part of Intel 7, so Intel won’t get the benefits of new process nodes here and the complexity of trying to launch a massive server part on such nodes. Meanwhile, Granite Rapids and Sierra Forest, which will be built on the Intel 3 process, remain scheduled for 2024.

Otherwise, the product updates embedded in Intel’s quarterly results are a pretty high-level overview of what’s to come, but it’s worth noting that Intel isn’t telling us anything new from its up-and-coming AXG GPU group. The latest news about the Rialto Bridge, Intel’s second-generation HPC accelerator, was that it wouldn’t start sampling until this year. Similarly, the Battlemage architecture for client GPUs seems to span between 2023 and his 2024.

Regarding Intel’s fabs, no significant changes have been announced to Intel’s schedule. Intel 4 is officially “manufacturing ready” and Intel 3 is on track. Meanwhile, Intel is making the first test chips for the 20A and 18A processes. To that end, Intel expects 2024 to kick off the high NA era of silicon lithography in earnest.

{kind=link}