As we begin our coverage of the tech industry’s first earnings season of the year, we’ll start, as usual, with Intel. The blue-hued blue chip is the first company to report results for the first quarter of 2023, with Intel following a rocky end to 2023 and a rather disappointing start to 2023. is picking up With client and server sales plummeting across the industry, at almost his once-a-year rate, Intel has focused on solidifying its hatch to weather this tough time, and the market’s Preparing for an eventual (albeit modest) turnaround. Later this year.

Intel’s revenue for the first quarter of 2023 was $11.7 billion, down a whopping 36% from the same period last year. As was the case in the fourth quarter, Intel is in the middle of a major industry recession that has hit revenue hard, and operating and net income even harder. Intel ended the quarter in the red on an operating income basis, losing $1.5 billion, and the company’s overall net loss was a staggering $2.8 billion on his GAAP basis.

| Intel First Quarter 2023 Results (GAAP) | ||||||

| Q1 2023 | Q4 2022 | Q1 2022 | year/year | |||

| Earnings | $11.7 billion | $14 billion | $18.4 billion | -36% | ||

| Operating income | -$1.5 billion | -$1.1 billion | $4.3 billion | -134% | ||

| net income | -$2.8 billion | -$661 million | $8.1 billion | -134% | ||

| gross profit | 34.2% | 39.2% | 50.4% | -16.2 points | ||

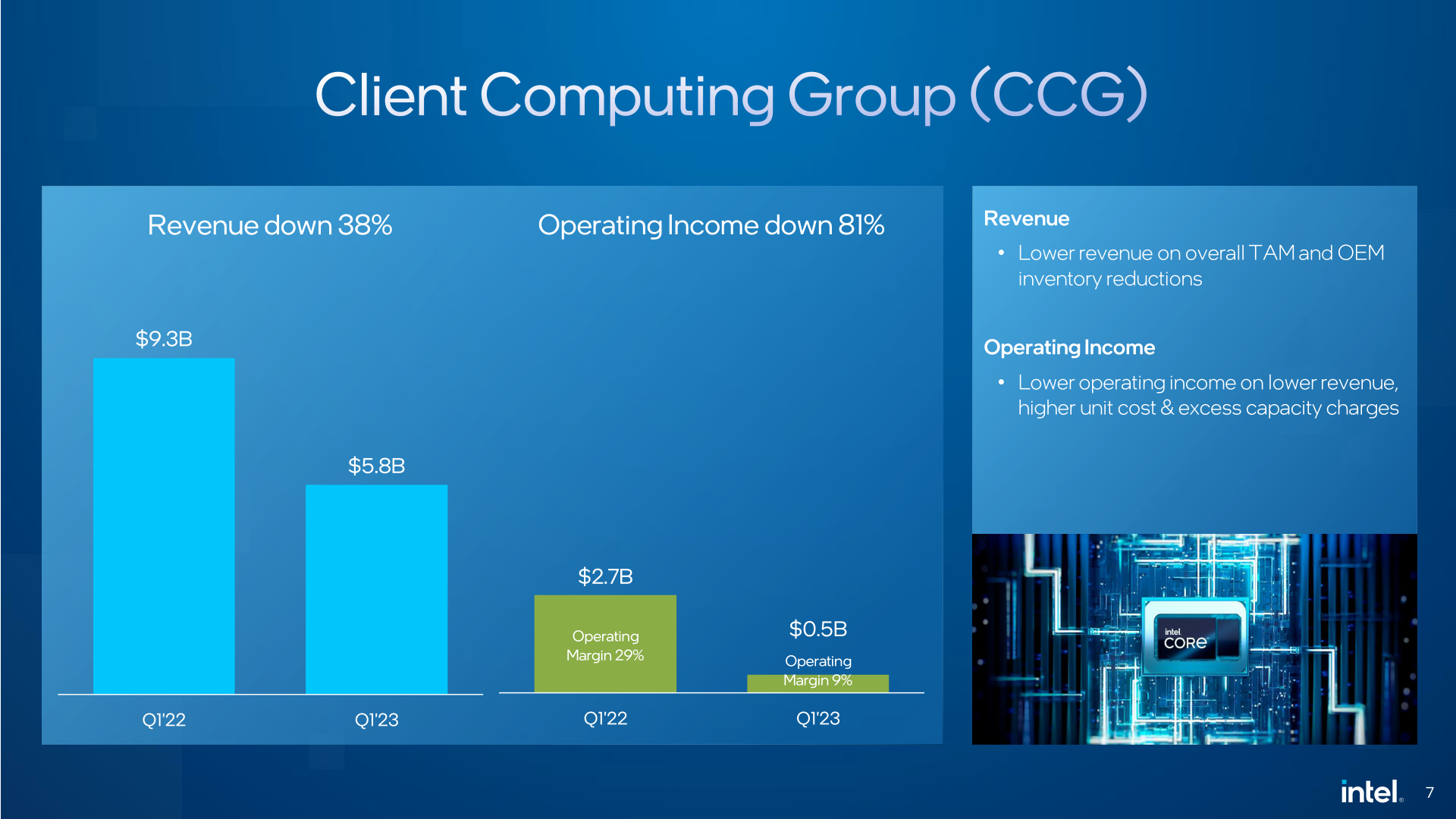

| Client Computing Group | $5.8 billion | $6.6 billion | $9.3 billion | -38% | ||

| Data center and AI group | $3.7 billion | $4.3 billion | $6 billion | -39% | ||

| Network and edge groups | $1.5 billion | $2.1 billion | $2.1 billion | -30% | ||

| mobile eye | $458 million | $565 million | $394 million | +16% | ||

| Intel Foundry Services | $118 million | $319 million | $156 million | -twenty four% | ||

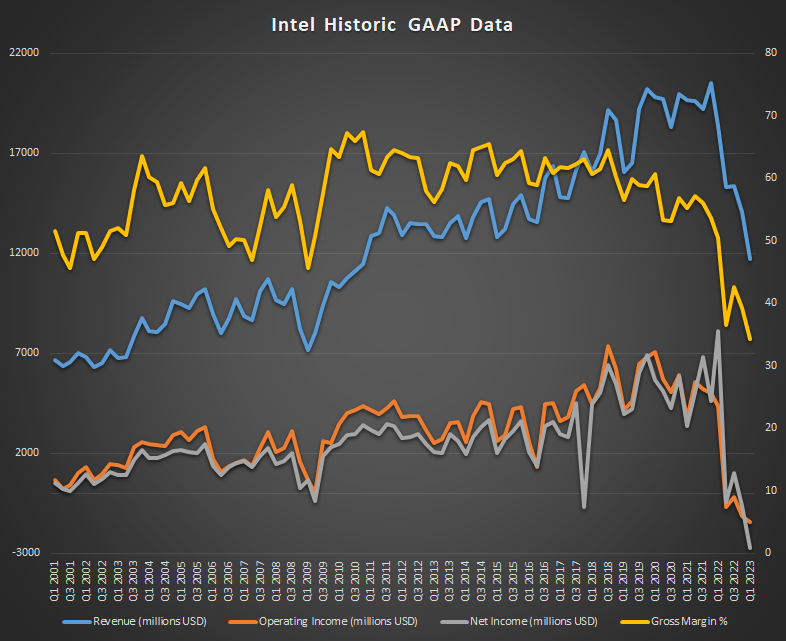

As a result, Q1 2023 turned out to be a record loss quarter for Intel, with the company posting its largest ever loss. Over the past 54 years, the company has had many ups and downs, but he has never lost more than $1 billion in a single quarter, let alone $2 billion. To be sure, some of this is structural, with restructuring charges, stock-based compensation charges, income taxes, and other non-core factors contributing to his GAAP net loss of more than $2 billion. But its scale is still staggering.

As a result, Intel’s highly prized gross margin dropped to just 34.2%, the lowest in at least 20 years.

Still, despite all of this, the quarter was better than expected for Intel. The company warned investors early on it was going to be brutal, and while Intel delivered on its promise, it has beaten earnings and EPS forecasts since the beginning of the quarter. While we are far from breaking out, there are some signs that we are nearing the bottom.

When we dive into individual segment performance, Client Computing Group (CCG) remains the company’s trailblazer. Unfortunately, he’s also one of the hardest-hit segments by the downturn in IT spending, with tech companies around the world recalling his PC sales dropping by more than 30% of his.

To that end, Intel posted client revenue of $5.8 billion in the quarter, down 38% from the year-ago quarter. Despite all of this, CCG maintained a positive operating margin, and with a 9% profit margin he trailed by $500 million. Looking at Intel’s detailed report, laptop sales dropped more than desktop sales, but both dropped significantly. At this point, Intel’s downstream OEM customers have exhausted their previously purchased inventory. This means Intel is selling far fewer chips than usual. Intel stopped providing his ASP information some time ago, so it’s unclear how much of a factor the change in chip prices is.

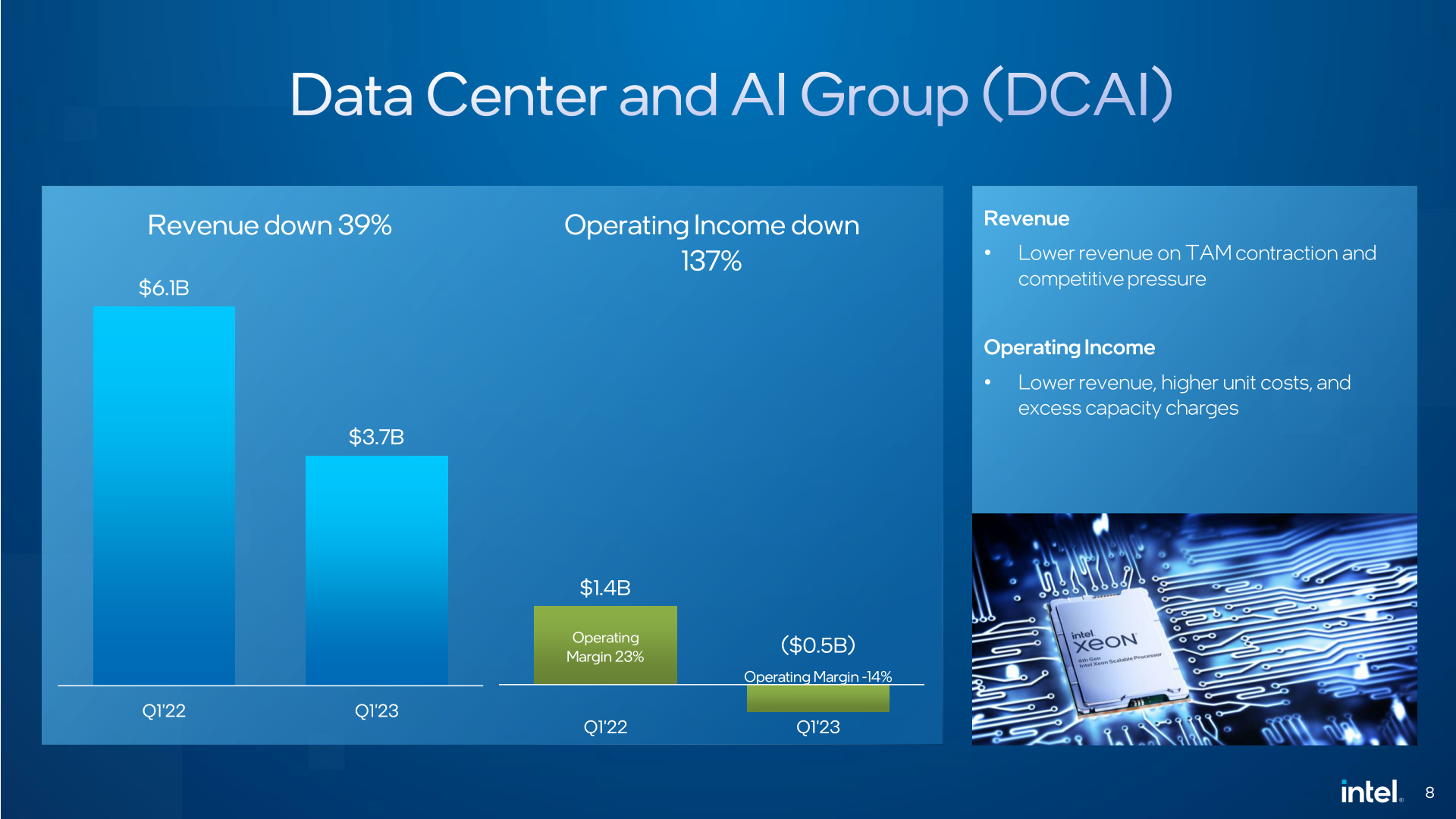

Moving forward, Intel’s Data Center and AI Group (DCAI) is recovering from its own problems. Intel is now shipping its long-awaited Sapphire Rapids processors in large numbers, and it’s still ramping up to meet its goal of selling one million chips by mid-year. Meanwhile, DCAI’s sales have softened even further than client sales, with revenues down 39% year-over-year, even as Sapphire Rapids finally exited.

Intel’s DCAI revenue for the quarter was just $3.7 billion. On an operational basis, this equates to his $518 million loss for the company. The fact that Intel lost money in the data center segment is notable, but not for good reason. The data center/server business has reconfigured many times over the past decade and has never lost money. check around, which seems correct. Despite being traditionally Intel’s most profitable business unit, Intel didn’t even find an operating profit for server components this quarter.

Complicating matters a bit is another organizational change within Intel. Accelerated Computing and Graphics Group (AXG), formerly a top-line business unit, split in late December and merged into the CCG and DCAI business units, each responsible for half of the business. The latest incarnation of AXG currently focuses only on the data center portion and is part of DCAI. I bring this up because, as a fledgling business unit, AXG itself is running an operating loss in 2022. Intel’s revised numbers show a similar year-over-year comparison with the revised business unit. To enable, the combined business unit shift reduced DCAI’s operating income by nearly $300 million in the first quarter of 2022. We have no way of knowing what the impact would have been in 2023, but it would be unlikely that AXG would have been a positive contributor to his DCAI’s profitability.

The last of Intel’s big groups is the Network and Edge Group (NEX), which covers Intel’s networking, connectivity, and IoT products, and where Intel records other silicon sales, such as Xeon SKUs for networking products. is. NEX was hit similarly to Intel’s other top-line groups, with revenue down 30% to $1.5 billion. That was enough of a drop to push NEX into the red, and he lost $300 million in the quarter. According to Intel CEO Pat Gelsinger’s comments, NEX’s customer base is undergoing destocking similar to some of its other chip units, which will continue for several more quarters.

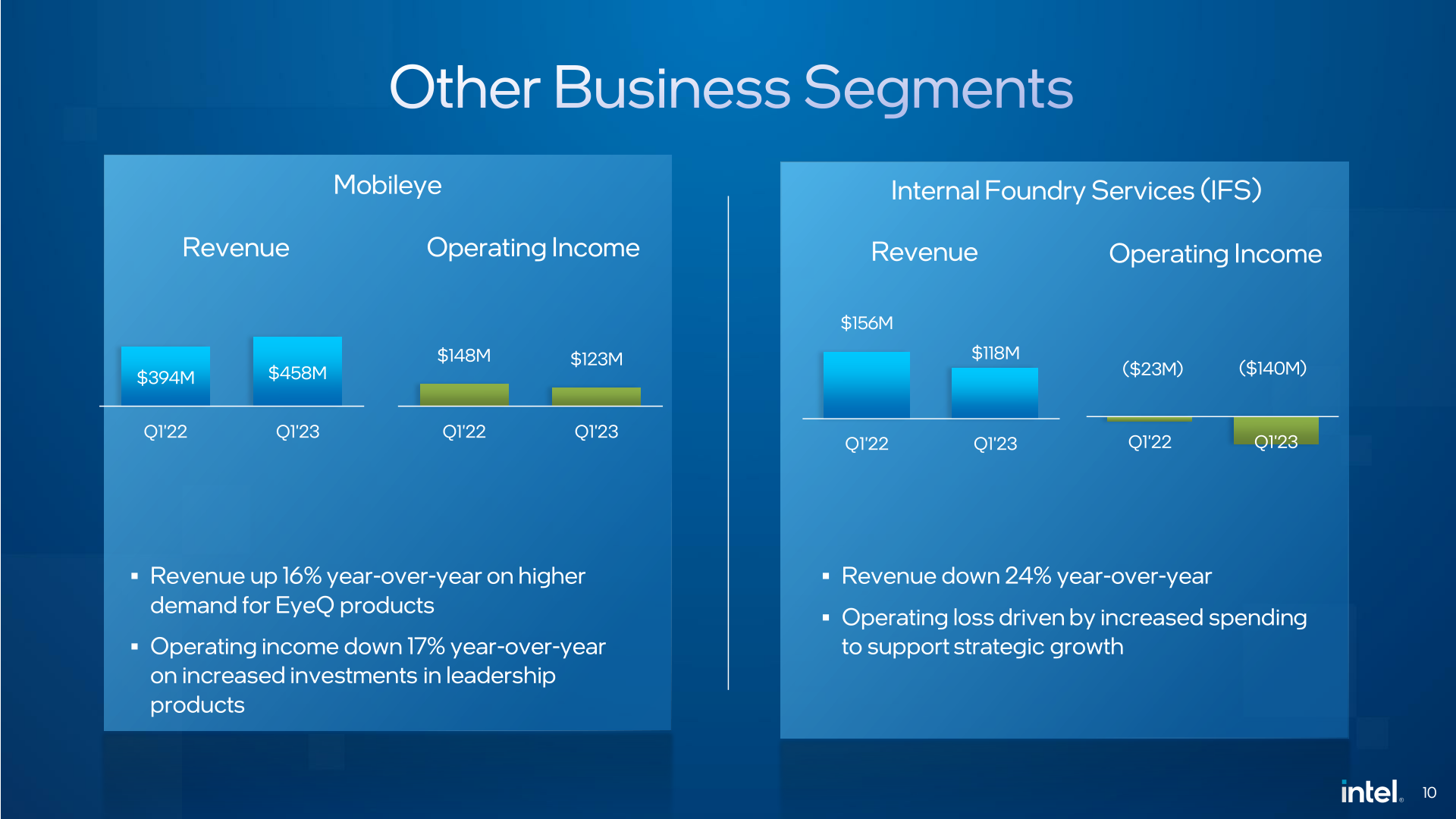

Rounding out Intel’s portfolio, Mobileye was the lone bright spot on Intel’s earnings report. The automotive group’s revenue rose 16% year-on-year, reaching a new quarterly record. Also, operating profit he fell 17%, but is still profitable. Meanwhile, Intel Foundry Services (IFS) was in the red, which is not unexpected as Intel is in the midst of a multi-year investment strategy to regain fab performance leadership. Despite a 24% year-over-year decline in revenue, Intel revealed that IFS has a long-term outlook and will continue to invest heavily.

Looking ahead, Intel shows that some of its business segments have bottomed out (or nearly bottomed out), but Q1 wasn’t the last bad quarter for Intel. The company forecasts his second-quarter 2023 revenue from $11.5 billion to $12.5 billion, a 22% year-over-year decline. Gross margins are also expected to decline further, with GAAP gross margins expected to be just 33.2%. As previously mentioned, the company expects a modest recovery in the second half, but still needs to get through the second quarter to get there.

Following the first quarter, Intel’s major overall initiatives remain unchanged in terms of both product plans and operating expenses. As announced last year, the company is working to cut costs significantly. Pat Gelsinger says Intel is “on track” toward his $3 billion cost savings in 2023, and will reach $10 billion in savings from $8 billion annually by the end of 2025. doing.

Otherwise, Intel isn’t planning any major product launches that would significantly change the status quo in its public roadmap for Q2. However, one bright spot in terms of hardware development is that Intel’s next-generation Intel 4 production process and associated Meteor Lake client CPUs have entered production with more to come throughout the year. This is a promising sign that Intel is on track, as in four years he needs to deliver five nodes to regain leadership in the fab market.

{kind=link}