Quantitative Tightening (QT) shrinks the Federal Reserve’s balance sheet. Substantial amounts of Treasury and agency mortgage-backed securities have been transferred to investors.

Current Fed policy is to use the QT as a tool to combat inflation and rising interest rates.

This is in contrast to quantitative easing, which has become more common over the past few years, where central banks print money to buy securities from the open market.

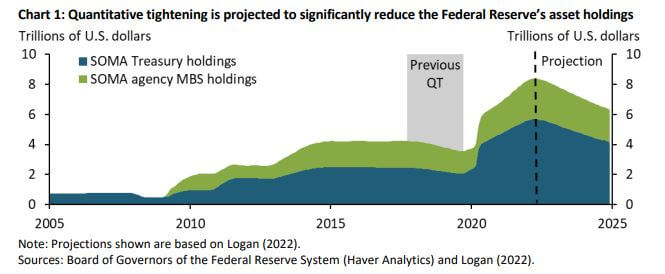

QT has not been US policy since 2017. According to macro data, this QT becomes more important when financial markets are stressed. The goal is to reduce the Fed’s $9 trillion balance sheet to counter surging inflation.

The Federal Reserve’s balance sheet, which stood at $4.2 trillion in 2019, had grown to a staggering $8.9 trillion by the end of May 2022 due to aggressive asset purchases during the Covid-19 pandemic. .

Between 2017 and 2019, the Fed cut its bond holdings by $650 billion. This year he began to see the effects of QT in September and data suggests that QT will be more extensive and aggressive than he was in 2017. The Fed could sell $95 billion of Treasuries and mortgage-backed securities based on forecasts of $2 or more. Trillion.

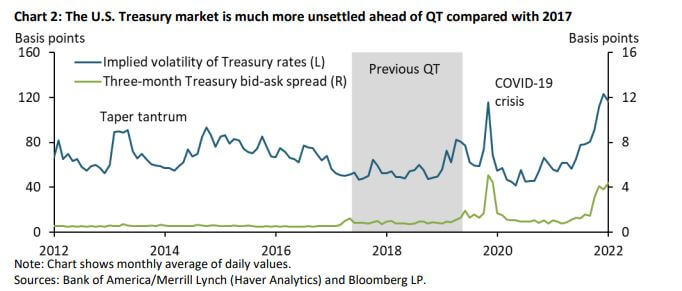

Additionally, the US Treasury market is also more volatile than in 2017. The blue line in the chart below shows the MOVE index, which measures the future volatility of Treasury yields.Volatility is well above period levelsis doing The period before the height of Covid-19 and the QT of 2017.

The green line represents a liquidity indicator, such as the bid-ask spread for US Treasuries. This spread is also rising, as is the pandemic level.

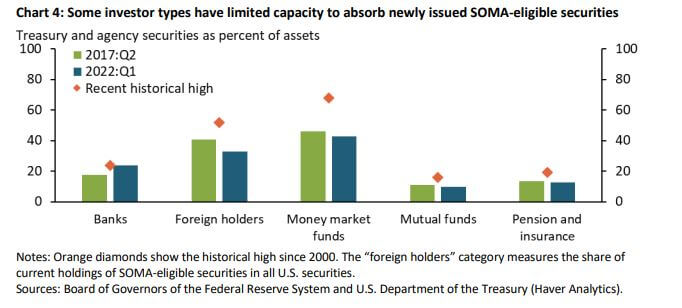

The chart below shows the largest share of SOMA-eligible securities held by each investor type since 2000. This data serves as a realization benchmark for the maximum absorptive capacity of the balance sheet. Foreign holders and money market funds (MMFs) may be able to absorb additional his SOMA eligible securities, albeit to a limited extent. But pensions and banks are almost full.

The share of foreign holders has declined since the global financial crisis as they have turned to buying gold instead. The Fed will need much higher yields for short term maturities. This indicates that this QT episode could be more disruptive than ever, mainly due to rising interest rates.

Bitcoin has no such monetary policy. There is no way to increase the supply without forking the entire network, eliminating the ability of any party to increase the Bitcoin money supply. Bitcoin is automated from a monetary policy perspective, and supply is directly related to hashrate and network difficulty. These mechanisms form part of the argument in favor of Bitcoin as a store of value and a long-term inflation hedge.

The crypto industry has followed the traditional stock market throughout 2022. But Bitcoin has never experienced a recession, his QT aggressive, or inflation. >2.3%, all of which are prevalent in today’s market. The next 12 months will be unprecedented territory for Bitcoin and a real test of its economic design.