Continuing our coverage of the Q1 2023 earnings season, Intel’s yang, AMD, has a dark side today. AMD, the second largest x86 chip and discrete GPU maker, has enjoyed growth in Intel’s lunch for the better part of the past two years, but like the rest of the tech industry, AMD is currently experiencing a slump in revenue as a company. I’m depressed significantly. Consumers will likewise reduce their spending on technology. So, like many other companies in the space, AMD has been gearing up for the first half of this year after beating out others with a modest profit in his fourth quarter of 2022. .

In the first quarter of 2023, AMD reported revenue of $5.4 billion, continuing the year-over-year decline it has experienced throughout the past few quarters. Overall, AMD’s top-line revenue was down 9% over his Q1 2022. That’s a much smaller decline than some of its competitors, but it’s also a situation artificially buoyed by the Xilinx acquisition, which closed in late Q1 2022. Revenue increased significantly year-on-year. AMD owning Xilinx for over a year.

The additional revenue and sales Xilinx brought to the table have changed AMD in some key ways, but haven’t helped stem the underlying sales decline facing the tech industry. As a result, the hit to AMD’s bottom line is enormous. Operating income dropped 115% to a negative $145 million, and net income similarly slipped into the red, down 118%, ultimately leaving him with a loss of $139 million. .

| AMD Q1 2023 Financial Results (GAAP) | ||||||

| Q1 2023 | Q1 2022 | Q4 2022 | year/year | |||

| Earnings | $5.4 billion | $5.9 billion | $5.6 billion | -9% | ||

| gross profit | 44% | 48% | 43% | -4.0pp | ||

| Operating income | -$145 million | $951 billion | -$149 million | -115% | ||

| net income | -$139 million | $786 million | $21 million | -118% | ||

| earnings per share | -$0.09 | $0.46 | $0.01 | -116% | ||

While far from rival Intel’s record-breaking losses, recent quarters remain an eyesore for the black team, which has enjoyed a business ramp-up for the past few years against the backdrop of the Zen renaissance. At least one silver lining is that AMD’s core businesses across the board remain profitable on a non-GAAP basis. His GAAP loss to AMD was primarily due to structural costs, particularly his $305 million in stock-based compensation, and his $823 million reduction in the amortization of acquired (Xilinx) intangible assets. These have all been very common refrains for many tech companies over the last few quarters. technology and is now slowly losing value.

| AMD Q1 2023 Report Segments | |||||

| Q1 2023 | Q1 2022 | Q4 2022 | |||

|

data center

|

|||||

| Earnings | $1.295 billion | $1,293 million | $1.665 billion | ||

| Operating income | $148 million | $427 million | $444 million | ||

|

client

|

|||||

| Earnings | $739 million | $2,124 million | $903 million | ||

| Operating income | -$172 million | $692 million | -$152 million | ||

|

game

|

|||||

| Earnings | $1,757 million | $1.875 billion | $1,644 million | ||

| Operating income | $314 million | $358 million | $266 million | ||

|

embedded

|

|||||

| Earnings | $1,562 million | $595 million | $1.397 billion | ||

| Operating income | $798 million | $277 million | $699 million | ||

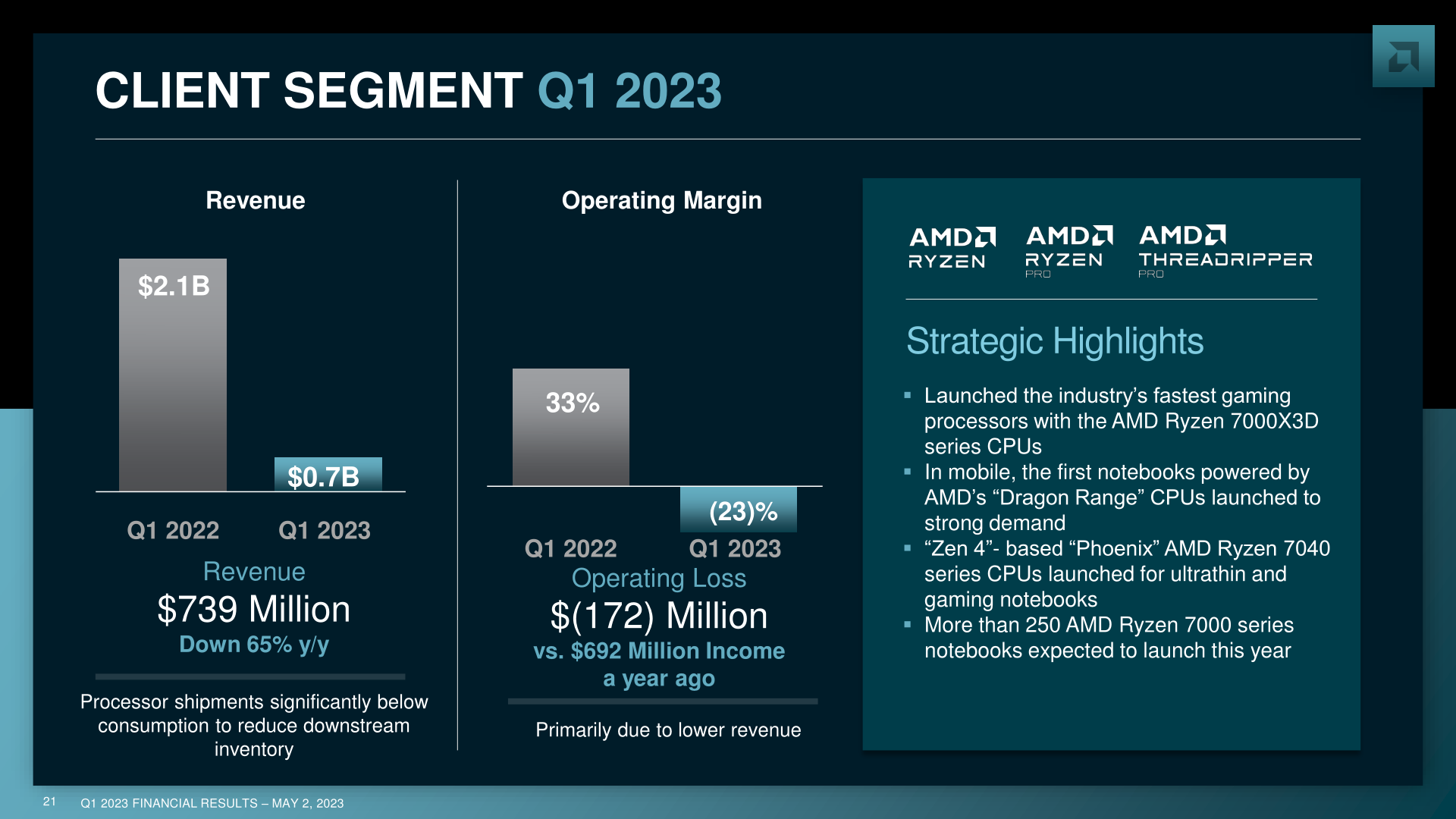

Moving on to AMD’s individual segment performance, we start with AMD’s client segment. This includes desktop and notebook CPU sales and chipsets. The complete collapse in client demand that began in the second half of this year has accelerated further in Q1 2023, resulting in AMD’s client revenue dropping a staggering 65%.

Overall, AMD posted just $739 million in client revenue for the quarter, its lowest ever. Client sales had the biggest drop across the technology industry, with AMD trailing others in this regard, as evidenced by a 65% drop in revenue when industry-wide client shipments fell by nearly 30-40%. of technology companies do far worse. This also put the segment’s operating profit in the red significantly, leaving AMD with a loss of $172 million in the division.

Like rival Intel, AMD’s OEM customers are working to reduce their inventories, exacerbating the decline in customer sales. So as long as the customer inventory bubble lasts, AMD has much less opportunity to sell chips. Client ASPs have also declined year-over-year, although AMD did not specify the extent. One of the good news here is that AMD believes it has finally hit the bottom of its Q1 client sales collapse. It means you can get through the worst and things will only get better from here.

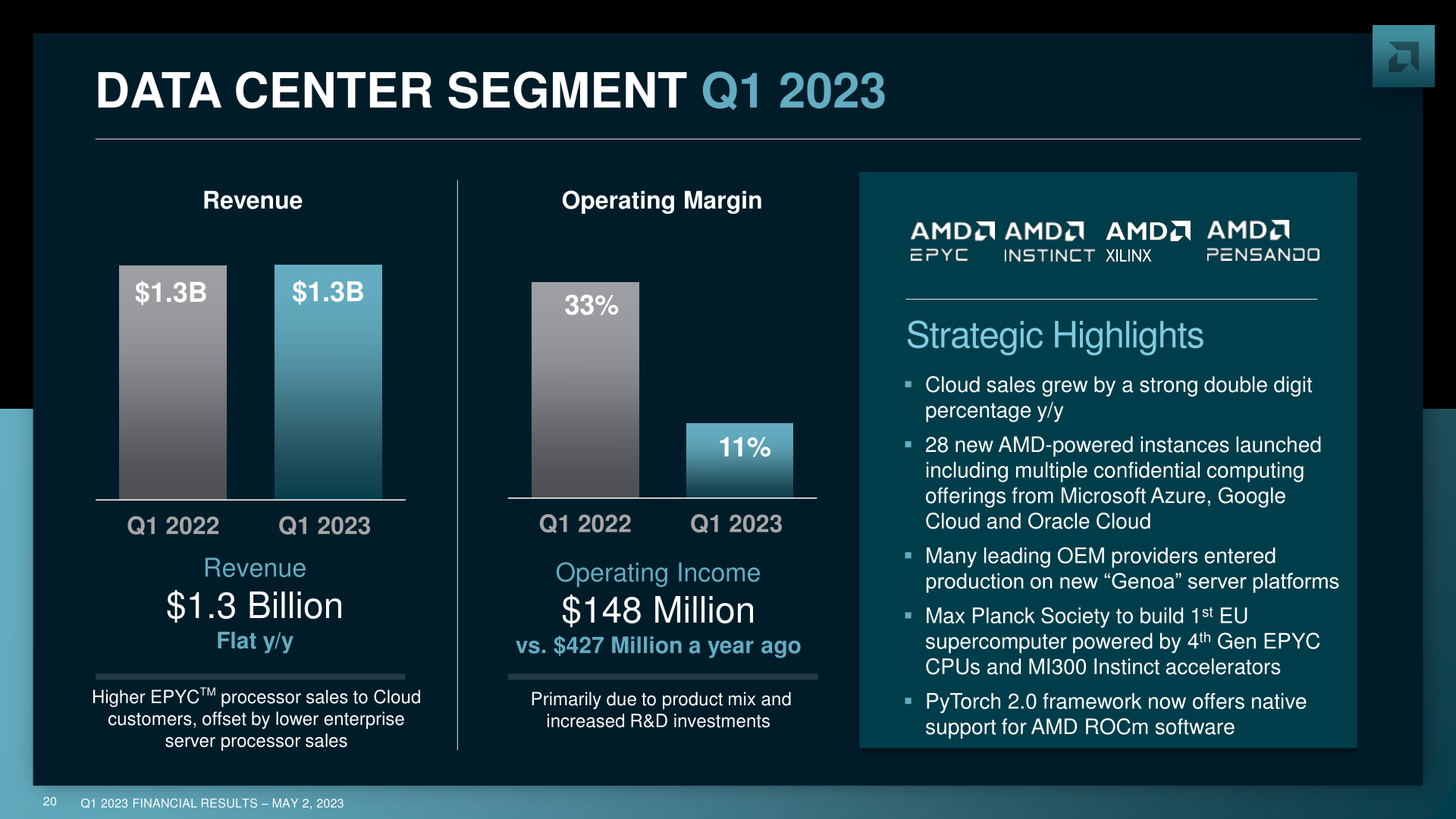

AMD’s data center segment, on the other hand, has had its own set of challenges in recent quarters as data center customers have reduced their spending as well. We are doing relatively well here due to our success in increasing our center market share. As a result, AMD’s data center revenue remained flat year over year at $1.3 billion.

Operating profit in this segment was hit, down 65% to $148 million, with margins of just 11%. Data center products are relatively profitable to begin with, which has allowed AMD to remain slightly profitable in this segment. Supporting the segment in the first quarter was higher EPYC CPU sales to cloud customers, which offset lower sales to enterprise customers.AMD’s new EPYC 9004 Genoa processors also shipped in the quarter. However, it does not appear to have had a significant impact on AMD’s revenue as customers are still ramping up server production. It is also worth noting that Essentially all products aimed at data center customers fall into this segment. to sell them.

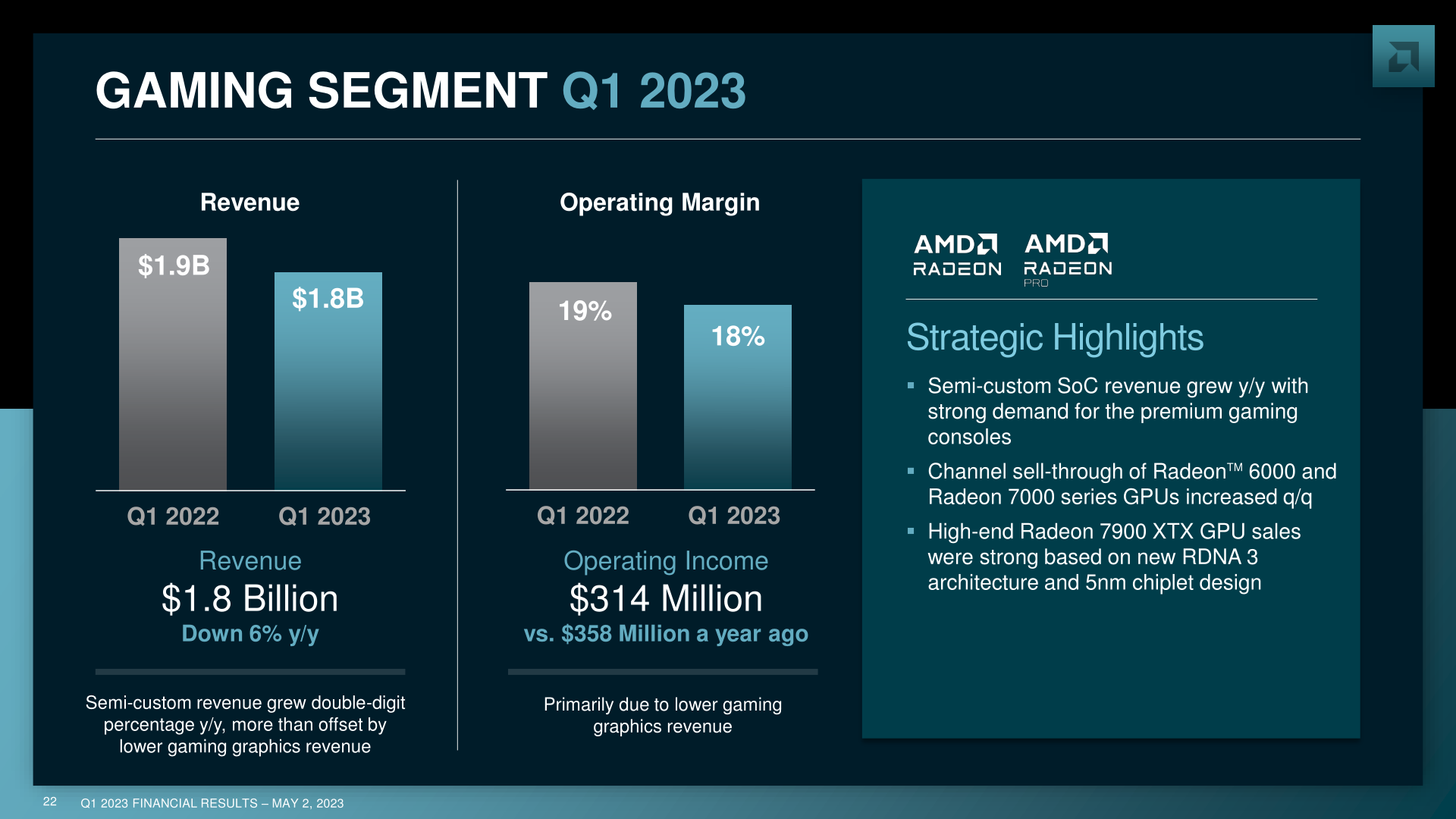

Moving on, AMD’s gaming segment turned out to be one of the strongest segments of the quarter. Client GPU and Semi-Custom SoC Group revenue declined year-over-year, but, importantly, operating margin declined only modestly.

For the quarter, AMD posted revenue of $1.8 billion in its Gaming segment, down 6% from the year-ago quarter. Operating income he was $314 million, down 12% year-over-year. Out of the limited breakout information provided by AMD, the company shows that client GPU revenue is declining by a significant amount, even though total unit sales are increasing. Preventing a significant drop in business is ‘double digits’ on the semi-custom side of the business as SoC sales for game consoles and other bespoke devices partially offset lower GPU revenues. is the growth of This is also why AMD’s operating profit in the segment has decreased somewhat as these semi-custom products get lower margins.

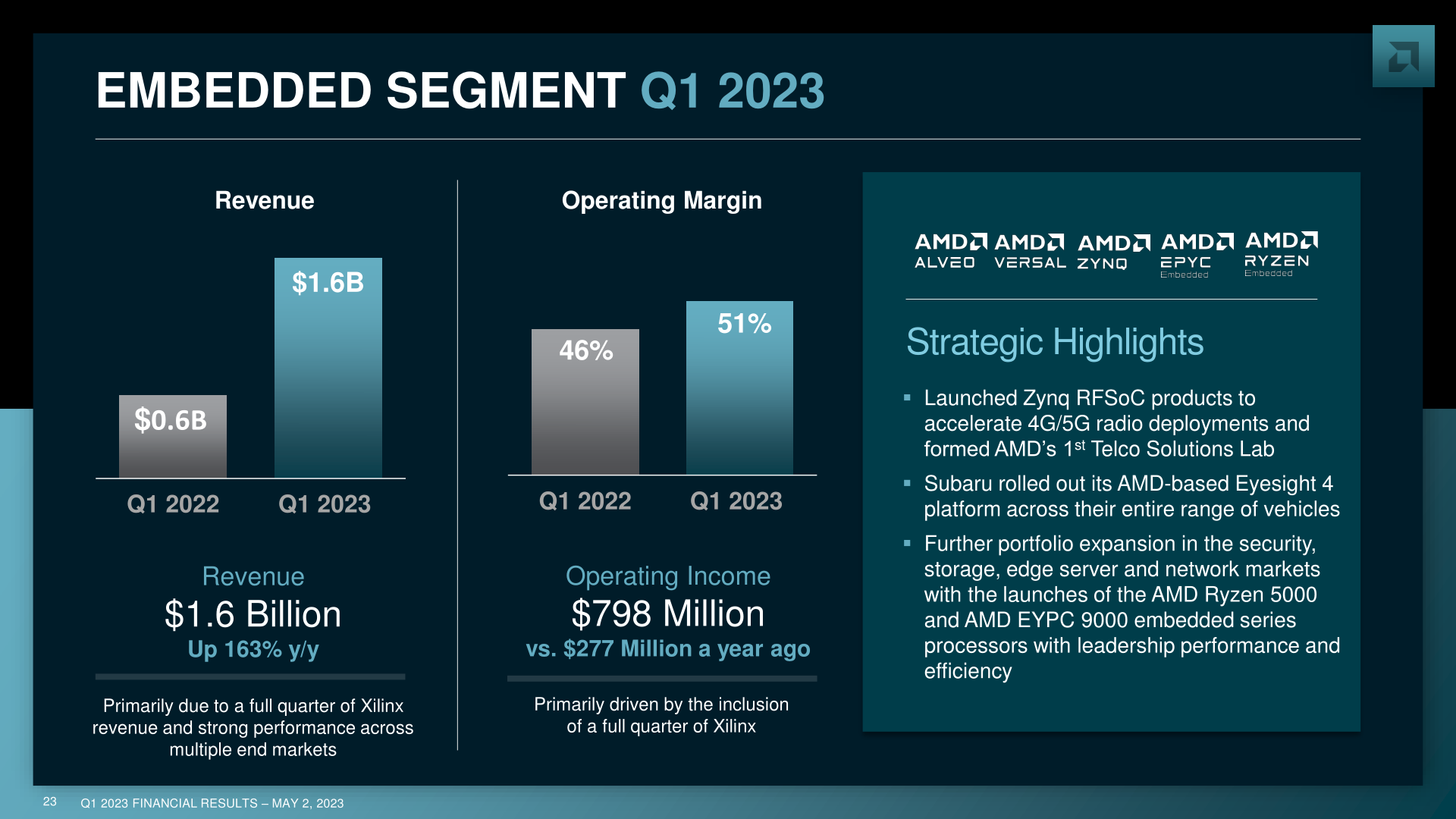

But the real winner of all of AMD’s reporting segments is the embedded segment, which covers the majority of Xilinx’s portfolio of FPGAs and other processors, as well as Ryzen and Radeon embedded SKUs. The segment has seen significant year-over-year growth in the last few quarters thanks to the Xilinx acquisition, and this is the last quarter for AMD to benefit from these acquisitions.

Embedded segment revenue was $1.6 billion and operating profit was $798 million in Q1 2023, up 163% and 188%, respectively. Despite the decline in technology spending, previous Xilinx products have proven relatively good in terms of sales consistency. But more importantly, embedded products have very high profit margins. The operating margin for this segment is 51%, far superior to any other AMD segment. This kind of consistency and market opportunity is a big part of why AMD wanted to acquire Xilinx in the first place, and keeping AMD a little more stable during this big tech spending downturn is a big part of that bet. is paying off.

The complete absorption of Xilinx and the subsequent decline in customer sales resulted in an interesting and relatively dramatic shift in AMD’s overall revenue share. A year ago, Client was AMD’s main business segment, but now it’s at the bottom. Even AMD’s data center segment lags behind both gaming and embedded. As former AnandTech editor Dr. Ian Cuttress put it, AMD has quickly become a “client last” company. This could change somewhat later this year as the client market recovers and the embedded market slows down a bit, but AMD may never be a client-first company.

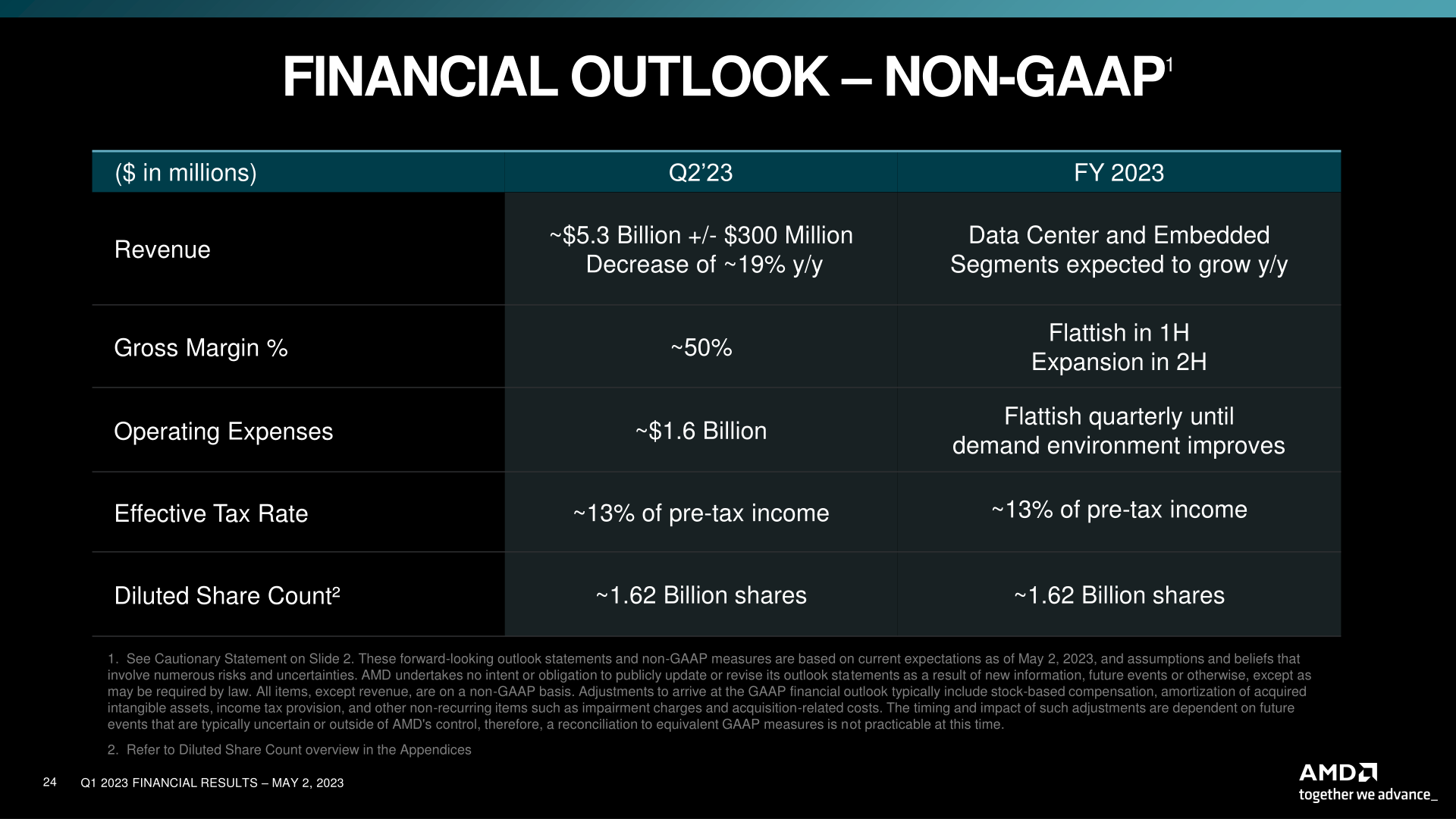

Going forward, AMD’s recovery plan looks a lot like the rest of the industry. If Q1 is a bottom, Q2 will be slightly better. To that end, AMD now forecasts second quarter revenue of $5.3 billion (+/- $300 million), a 19% year-over-year decline. No real recovery in client and data center space is expected until later this year, when AMD hopes to resume moderate growth in these segments.

In the meantime AMD is already gearing up for its turnaround. AMD said in its earnings report that product inventory increased slightly on a quarterly basis to $4.2 billion. This is done in anticipation of new data centers and client product growth at leading edge process nodes. It’s also not a good look at a time when customers themselves are destocking chips, but it reflects the longer time it takes to launch new products.

Finally, outside of direct financial concerns, the latest revenue cycle also makes AI products a little more difficult to explain. AMD makes extra effort to advance AI commitments and current product stack, buoyed by anxious shareholders eyeing higher margins and growth opportunities for NVIDIA and other AI-adjacent rivals have paid for In some ways, this is an effort to calm investors down until the Instinct MI300 ships later this year, which should be AMD’s biggest chance to enter the high-end AI training/inference market. but also reflects growing interest from the company. As pointed out on AMD’s conference call, former Xilinx CEO Victor Peng has recently taken charge of all of AMD’s AI efforts. So while AMD hasn’t announced a new AI roadmap, it’s clear that they’re looking to leverage Xilinx and Peng’s expertise in this space to improve their position in the long run.

{kind=link}