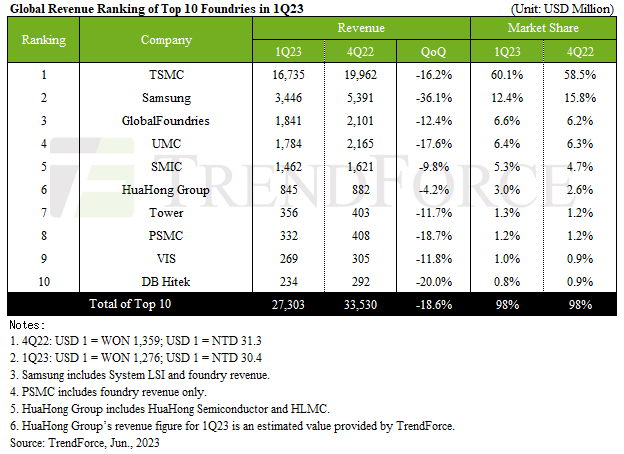

According to the latest report, the top 10 chip contract makers’ sales in the first quarter of 2023 fell 14.6% year-on-year and 18.6% quarter-on-quarter. trend force. The market intelligence firm attributed the decline in foundry sales to continued weakness in end-market demand and seasonality. TSMC and Samsung Foundry held on to the top spot, but GlobalFoundries overtook UMC for the first time in a long time and returned to third place.

According to TrendForce data, the world’s 10 largest foundries reported revenue of $27.3 billion in the first quarter of 2023, down 14.6% year-over-year (YoY) and down 18.6% quarter-over-quarter (QoQ). became. The decline in sales was driven by weakening demand for mass-market applications that use cutting-edge manufacturing technology, such as client PCs and smartphones, notably at his TSMC and Samsung Foundry. Meanwhile, UMC and DB Hitek were hit even harder than TSMC.

TSMCThe world’s largest chip contract manufacturer with a 60.1% revenue share, posted a profit of $16.74 billion, reflecting a 16.2% quarter-on-quarter decline and a 4.5% year-over-year decline. According to TrendForce, TSMC’s N7 (7nm class) and N5 (5nm class) process technologies have been underutilized due to sluggish demand for client PCs and smartphones. As a result, TSMC’s N7 family production node revenue fell by 20%, while foundry revenue from its N5 manufacturing technology lineup fell by 17%.

Urgent orders in the second quarter could be a brief relief for TSMC, but continued low facility utilization will continue to push revenue down, albeit more slowly than in the first quarter, TrendForce said. I think it will continue. TSMC expects second quarter earnings to be lower than first quarter, mainly due to seasonality and market uncertainty.

samsung foundry According to TrendForce, the company was hit by lower utilization rates at both its 200mm and 300mm fabs, resulting in an industry-best first-quarter sales decline of 36.1% quarter-on-quarter and a year-on-year decline of 35.25%. It has dropped to $3.45 billion. Market researchers now expect the Samsung foundry to pick up additional orders for certain parts at irregular intervals in the second quarter. Still, these orders are expected to be driven by short-term restocking and may not necessarily signal a resurgence in end-market demand. TrendForce also believes that an increase in orders for SF3E (3nm class) chips will also be a profit driver for Samsung’s contract chip manufacturing division.

global foundriesThe first quarter 2023 total was $1.84 billion, down 12.4% sequentially and down 5.2% year-over-year. GlobalFoundries focuses on specialty process technologies, serving sectors such as automotive, aerospace, defense, IoT and industrial where demand is relatively stable. This sustained stability helped GlobalFoundries overtake his UMC and secure his third place in the Q1 revenue rankings. Regarding the second quarter forecast, GF expects earnings to remain in line with the first quarter, benefiting from stable orders and continued capacity.

UMC Q1 2023 revenue was $1.78 billion, down 17.6% sequentially and down 21.4% year-over-year. TrendForce claims that this reduction is particularly pronounced for the 28/22 nm and 40 nm processes, each with a minimum of 20% reduction. The company expects 200mm fab utilization to drop below 60% in Q2 2023 as customer orders for PMICs and MCUs fall. In contrast, 300 mm fab utilization is expected to benefit from immediate orders for 28/22 nm products such as TV SoCs and timing controllers for LCD panels, with utilization expected to be 80%. Given that ASP remains stable, UMC expects sales to maintain current levels or increase slightly in the next quarter.

SMICIncome in Q1 2023 reached $1.46 billion, down 9.8% from the prior quarter and down 20.8% from Q1 2022. Interestingly, foundry demand for his 300 mm wafer processing services remained steady, up 1%. According to TrendForce, the company’s 200mm fab revenue plummeted 30% quarter-on-quarter. Analysts believe the steady orders for 300mm were supported by a diversified product portfolio and domestic demand in China. TrendForce expects SMIC to continue to benefit from increased orders for products such as driver ICs and NOR flash, maintaining its dominance from Chinese demand.

TrendForce predicts top 10 foundry revenues to decline further in Q2 2023. The supply chain is expected to gradually build up inventories in response to peak season demand in the second half of 2023, but slowing consumption and inventory build-up have made stockpiling more cautious. As a result, the market intelligence firm expects a relatively stable second quarter for foundries, with only a modest increase in capacity utilization. However, rush orders for some products such as TV SoC, WiFi 6/6E, and TDDI can significantly increase factory utilization.

sauce: trend force

{kind=link}