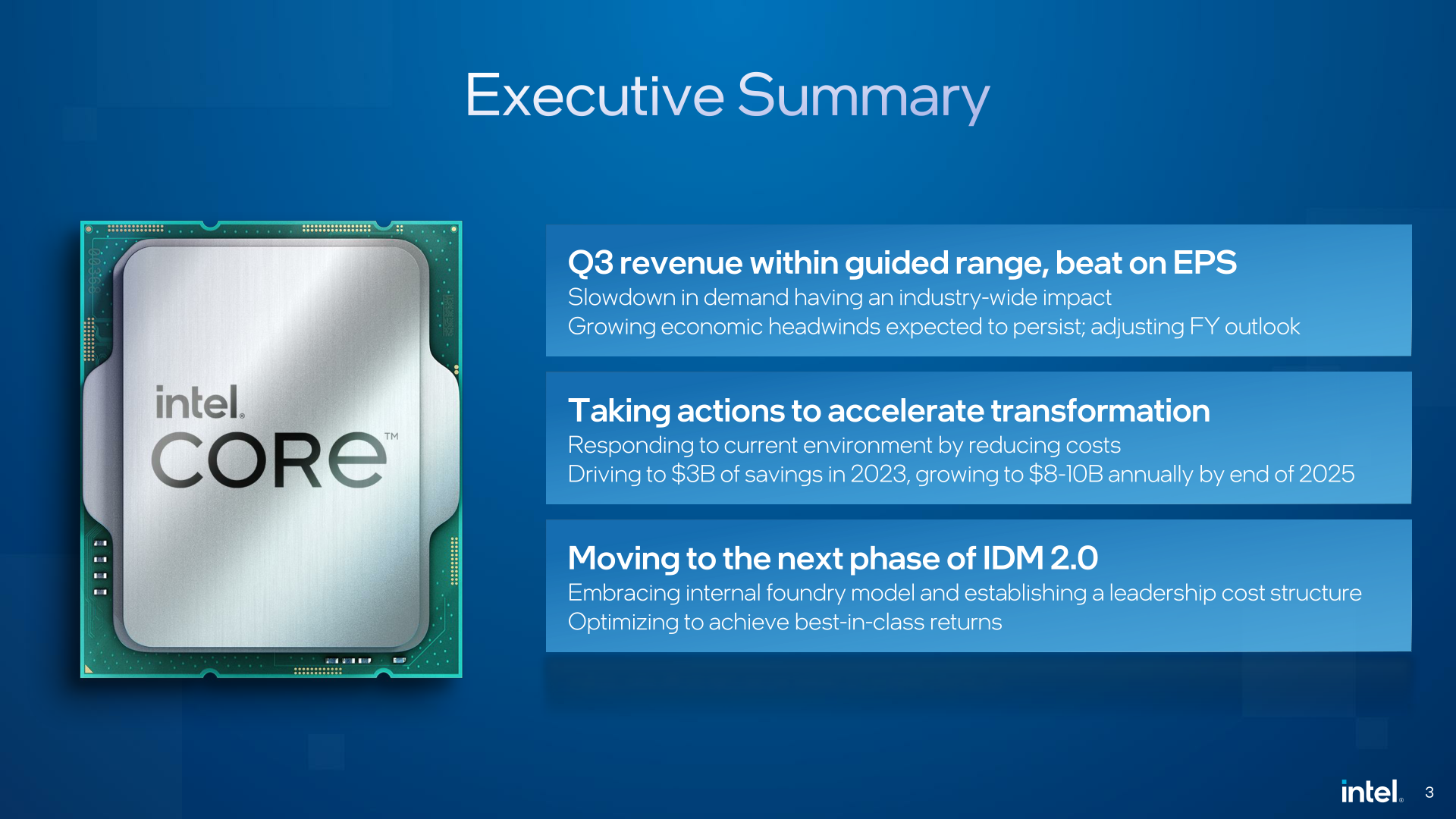

Always an interesting topic by default, corporate earnings reports in the tech industry have become especially important in recent months. As the industry prepares to weather what is expected to be the biggest demand drop in years. Intel’s brutal Q2 2022 report found the company losing on his GAAP basis for the first time in five years, but AMD and others issued earnings warnings ahead. Since then, it seems to have heralded what is to come for the largest industry. of its own third quarter report. As such, Intel is likely to once again become a barometer of the tech industry’s performance over the past three months, as the first major tech company to release a full Q3 2022 earnings report.

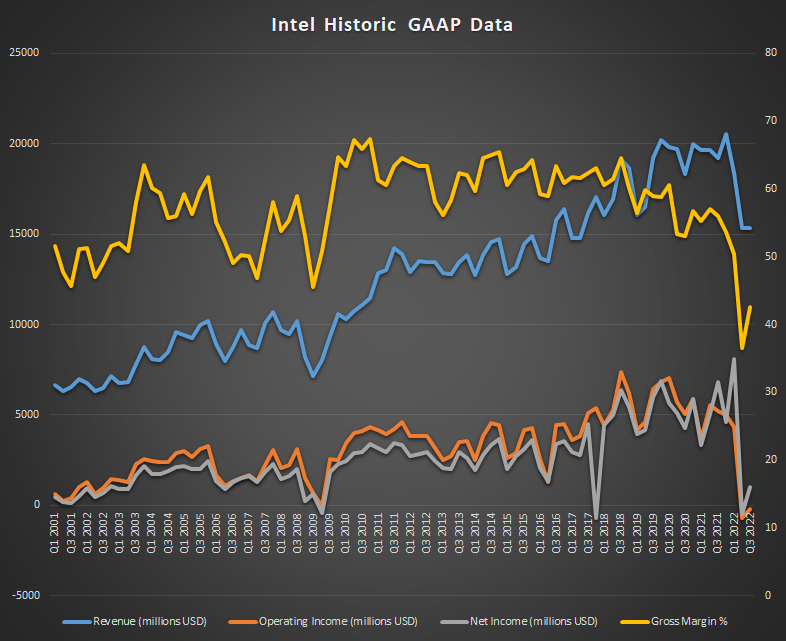

For the third quarter of 2022, Intel reported revenue of $15.3 billion. This is a decrease of $3.9 billion he from the same period last year. Compared to Intel’s second-quarter Hash report, the company is back in the black with net income in the billions, which is still well below historical standards. In fact, the company is still operating at a loss (GAAP) with an operating income of -$175 million. For the third quarter at least, Intel’s tax picture looks to be turning positive, with the company recording his $1.2 billion tax benefit.

| Intel Third Quarter 2022 Financial Results (GAAP) | |||||

| Q3 2022 | Q2 2022 | Q3 2021 | |||

| Earnings | $15.3 billion | $15.3 billion | $19.2 billion | ||

| Operating income | -$175 million | -$700 million | $5.2 billion | ||

| Net income | billion dollars | -$454 million | $6.8 billion | ||

| gross profit | 42.6% | 36.5% | 56.0% | ||

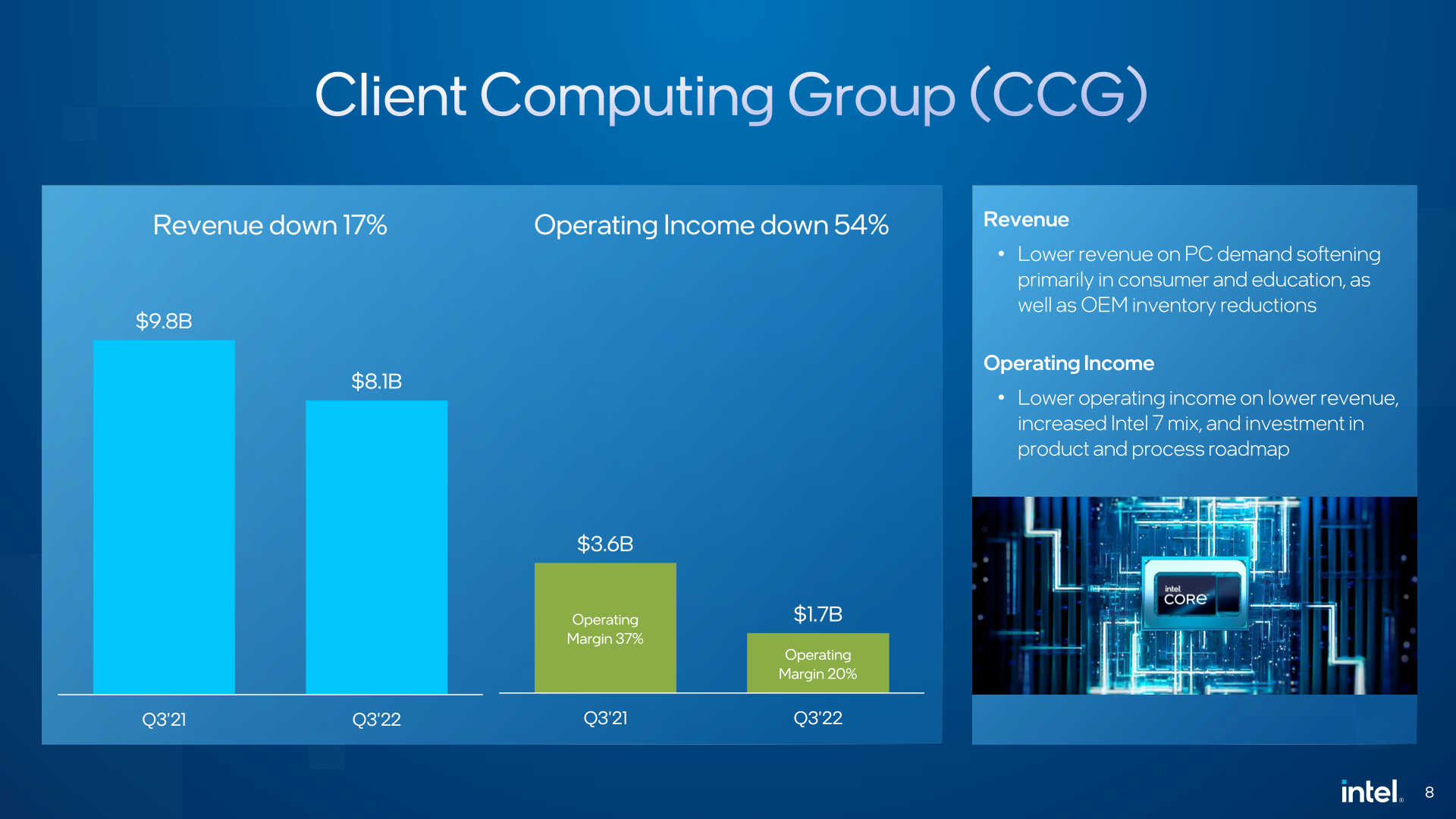

| Client Compute Group Revenue | $8.1 billion | +5% | -17% | ||

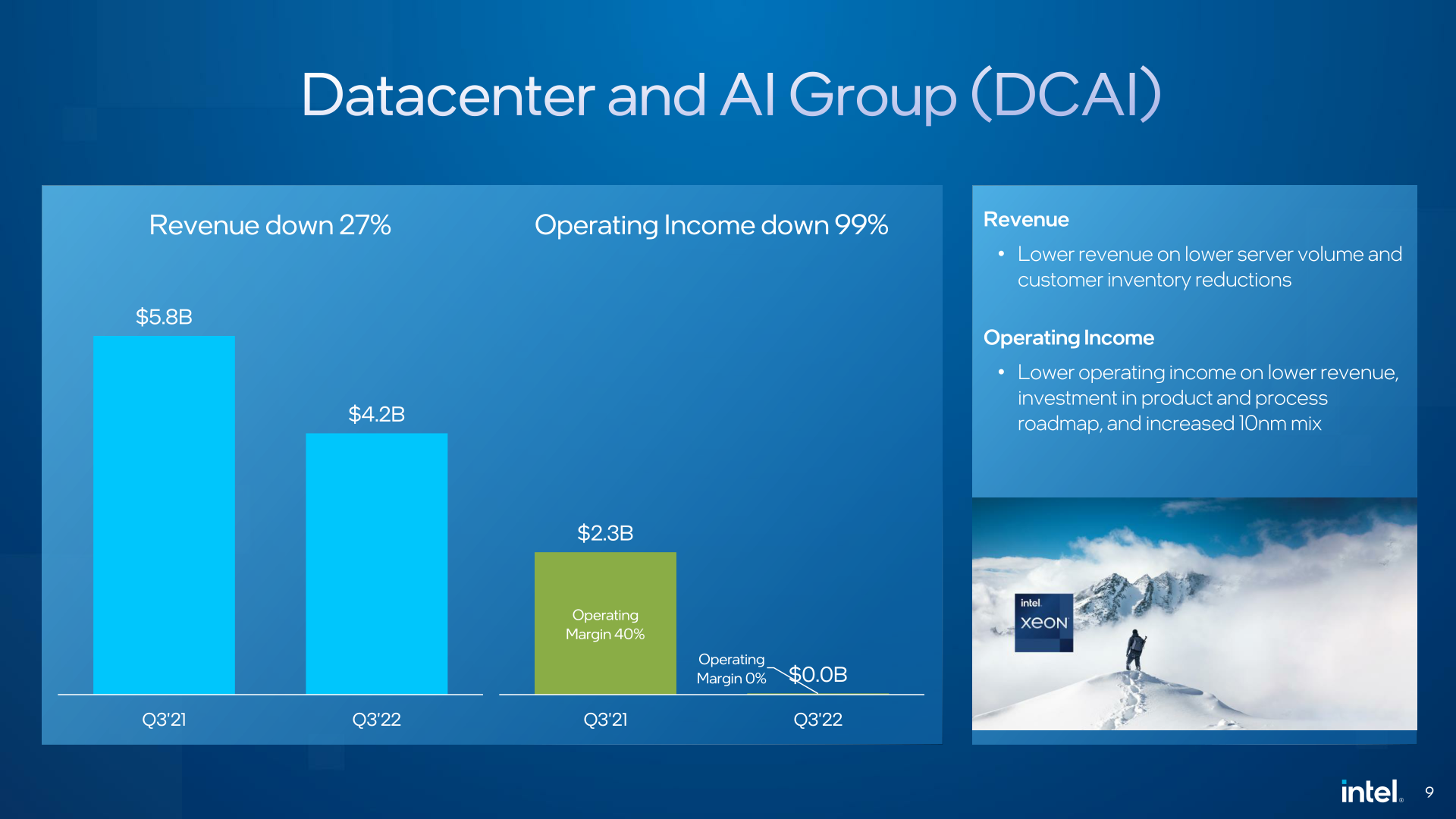

| Data Center & AI Group Revenue | $4.2 billion | -9% | -27% | ||

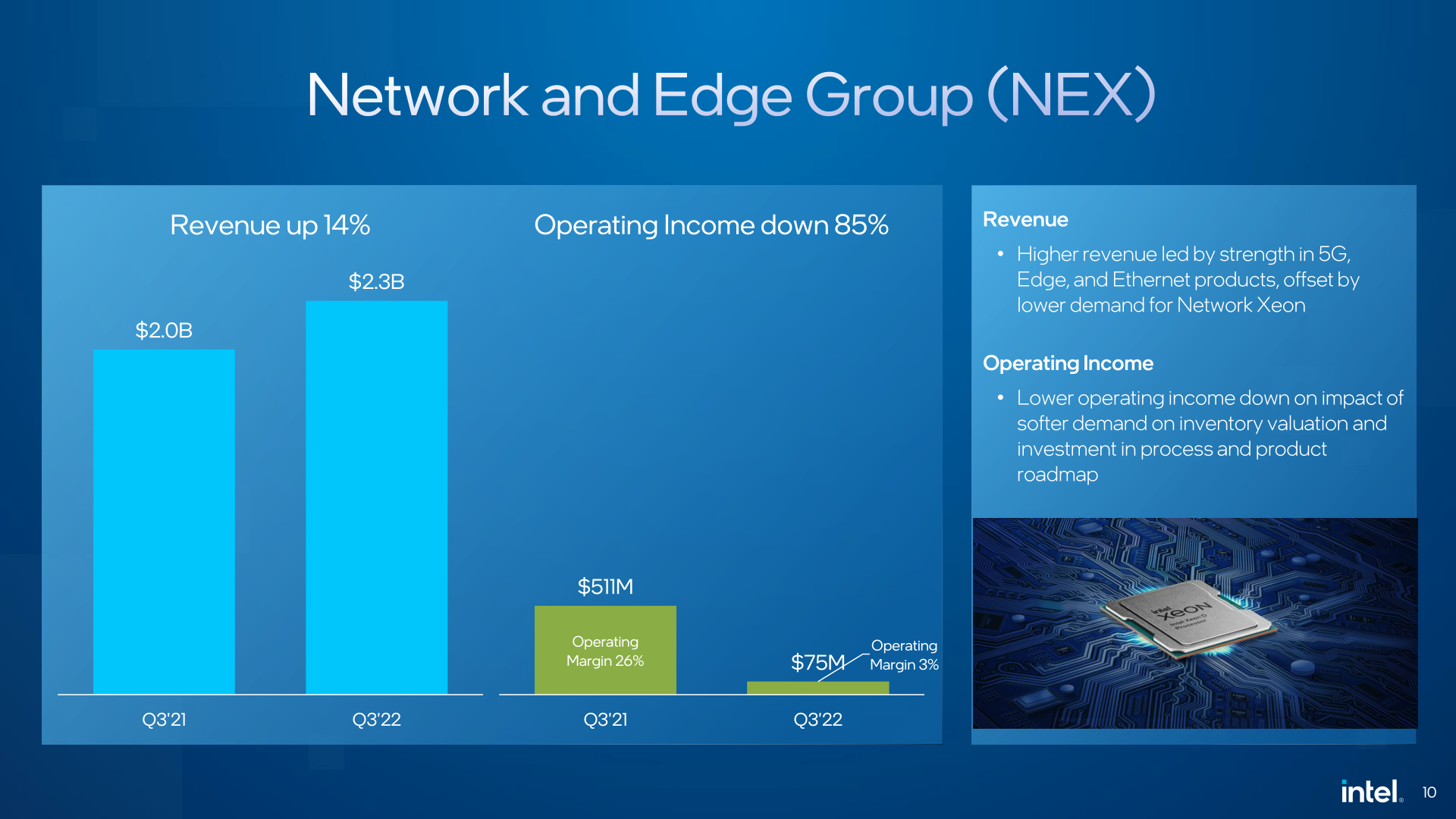

| Network & Edge Group Earnings | $2.3 billion | Flat | +14% | ||

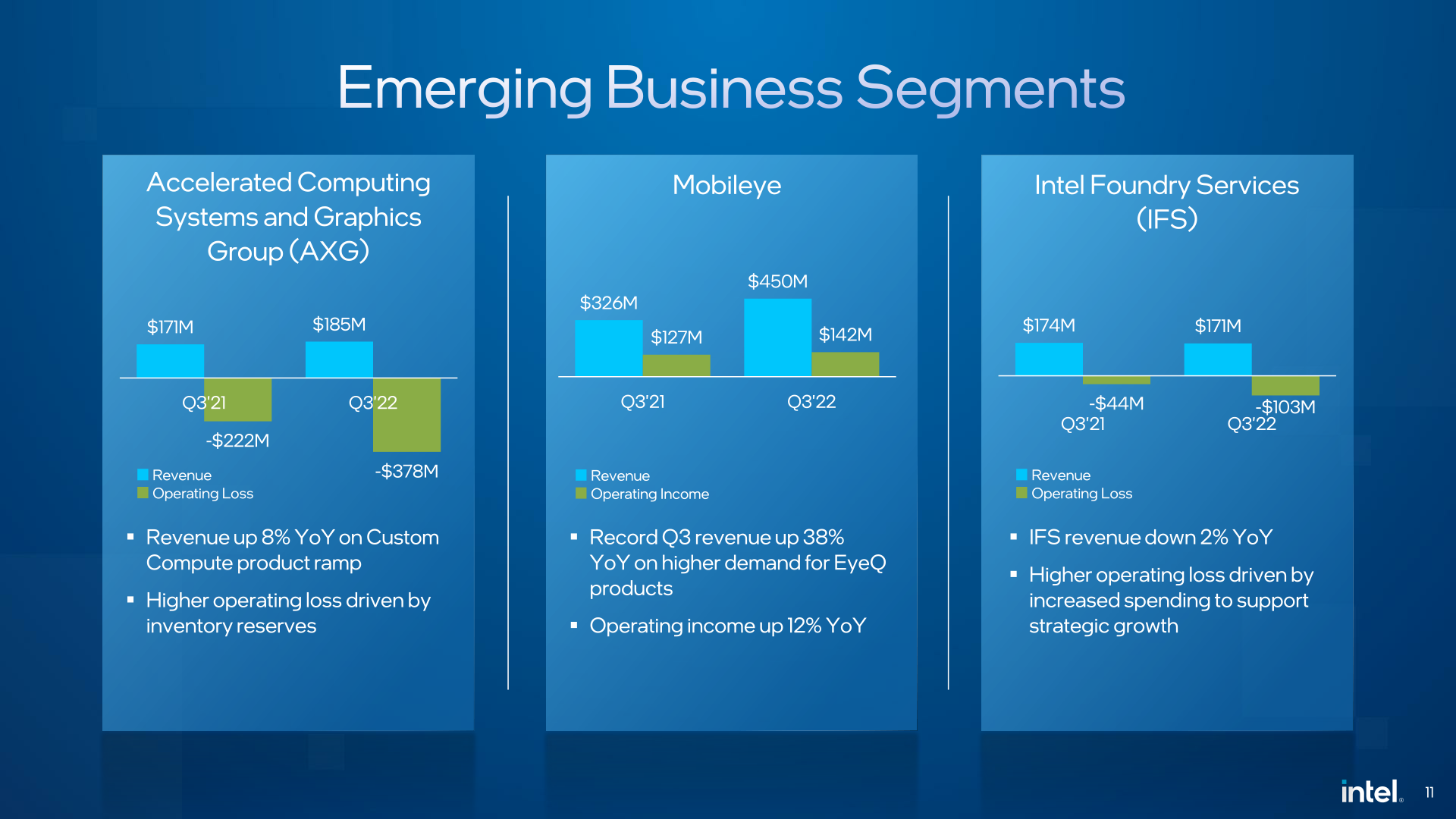

| Accelerated Computing Systems and Graphics Group Earnings | $185 million | -1% | +8% | ||

| mobile eye | $450 million | -2% | +38% | ||

| Intel Foundry Services Revenue | $171 million | +40% | -2% | ||

That said, the company appears to be slowly turning a corner after Intel’s second quarter hit. Gross margin improved to 42.6%. That’s still below Intel’s historical (or recent) average, but at least high enough to push the company’s operating profit closer to positive numbers.

These numbers also reflect some one-time charges, notably the $664 million restructuring charge Intel is currently taking to reduce ongoing costs (headcount reductions). We’ll talk more about Intel’s future predictions and actions later, but in short, Intel may have gone through the worst of it, but Intel is again lowering its earnings forecasts for this year as a bust cycle. What the PC industry as a whole is going through is not over yet.

When broken down by Intel’s individual business groups, both of Intel’s major groups, CCG and DCAI, saw significant year-over-year declines. Note that this is still the first year of Intel’s reorganized business group. So Intel had to provide a year-over-year comparison of how the new group would have performed if it had been in place last year.

Starting with CCG as usual, Intel’s customer group recorded $8.1B in revenue. This is down 17% from the same period last year. CCG, which is most exposed to consumer market collapse, has seen the impact of OEMs ordering fewer chips thanks to their own large inventories as consumer and education system sales slow. I am receiving The operating profit margin is also declining. This is due to lower revenue due to expenses and Intel’s continued investment in product development.

In the short term, Intel expects the total addressable market (TAM) of the PC market to shrink to the ‘mid-to-late teens’ of 2022, a blow that will continue throughout the year. Intel’s 13 recent launchesth Generational Core (Raptor Lake) parts will help spark new demand, but not enough to fully offset the overall decline in the much larger PC market.

As for Intel’s Data Center and AI Group (DCAI), the company suffered an even bigger revenue hit. In the third quarter, Intel posted his $4.2 billion in DCAI revenue, down 27% from the same period last year.

This revenue decline nearly wiped out the group’s operating profitability, with Intel recording a group operating profit of $0 billion and an operating margin of 0%. Intel attributes this to lower server/AI part sales as customer demand weakens, but with more and more server processors shipping on the Intel 7 and 10ESF processes, Intel’s Relative costs are rising.

Intel, of course, is about to ship 4, which has been significantly delayed.th Generation Xeon Scalable (Sapphire Rapids) processors. Therefore, along with economic factors, customers are eagerly awaiting Intel’s next-generation hardware. According to the company, they officially shipped a “massive” Sapphire Rapids SKU in Q3, but the chip is still far from getting ARK entry, so it’s clear it’s not fully launched yet. Despite this, Sapphire Rapids has reached PRQ (Product Release Qualification). This is where Intel is fully satisfied that yields are high enough and performance is suitable for silicon being produced for retail production.

Intel’s last billion-dollar business, the Network and Edge group (NEX), is one of the real bright spots in this quarter’s earnings call. NEX revenue increased 14% year-over-year to reach $2.3 billion.

Still, operating profit declined significantly, down 85% to $75 million. Ultimately, Intel saw strong demand for his more dedicated networking products such as 5G and Ethernet, while his Xeon products sold as part of this segment suffered a decline in demand.

Finally, Intel’s “upstart” sub-billion dollar group was a mixed bag. AXG’s revenue is up slightly, but the group will continue to lose money for years to come until Intel fully enters the market and ships client and server GPUs in bulk. Intel Foundry Services is in a similar boat, with Intel continuing to make the necessary investments to enter the contract fab market in a big way. Otherwise, Mobileye not only turned a profit, but grew year over year. Intel just completed its Mobileye IPO this week, making it no longer a wholly owned subsidiary of Intel, but it will still have a positive impact on Intel’s earnings sheet as it still owns the majority of the spinoff.

So what’s next for Intel from here? The company thinks it’s already weathered the worst of the quarter in terms of profitability, but Intel is preparing itself and its investments for the rest of this downturn cycle. Both homes need to be prepared. Recession.

As far as Intel’s own forecast goes, the company is currently seeking to bring in $63 billion to $64 billion in revenue in fiscal 2022, which is $2 billion to $4 billion less than its previous (Q2) forecast. That means the market will be weaker than Intel thought at the end of Q2. If the new predictions come true, annual earnings will fall by 14% to 16% from 2021.

This also means that Intel’s gross margin won’t fully recover this year. Annual gross margin is now projected to reach 47.5%, especially in the fourth quarter he is expected to reach 45%. Intel still expects to be profitable, but it’s not out of the picture just yet, with Q4 revenue expected to fall by up to 28% year-over-year.

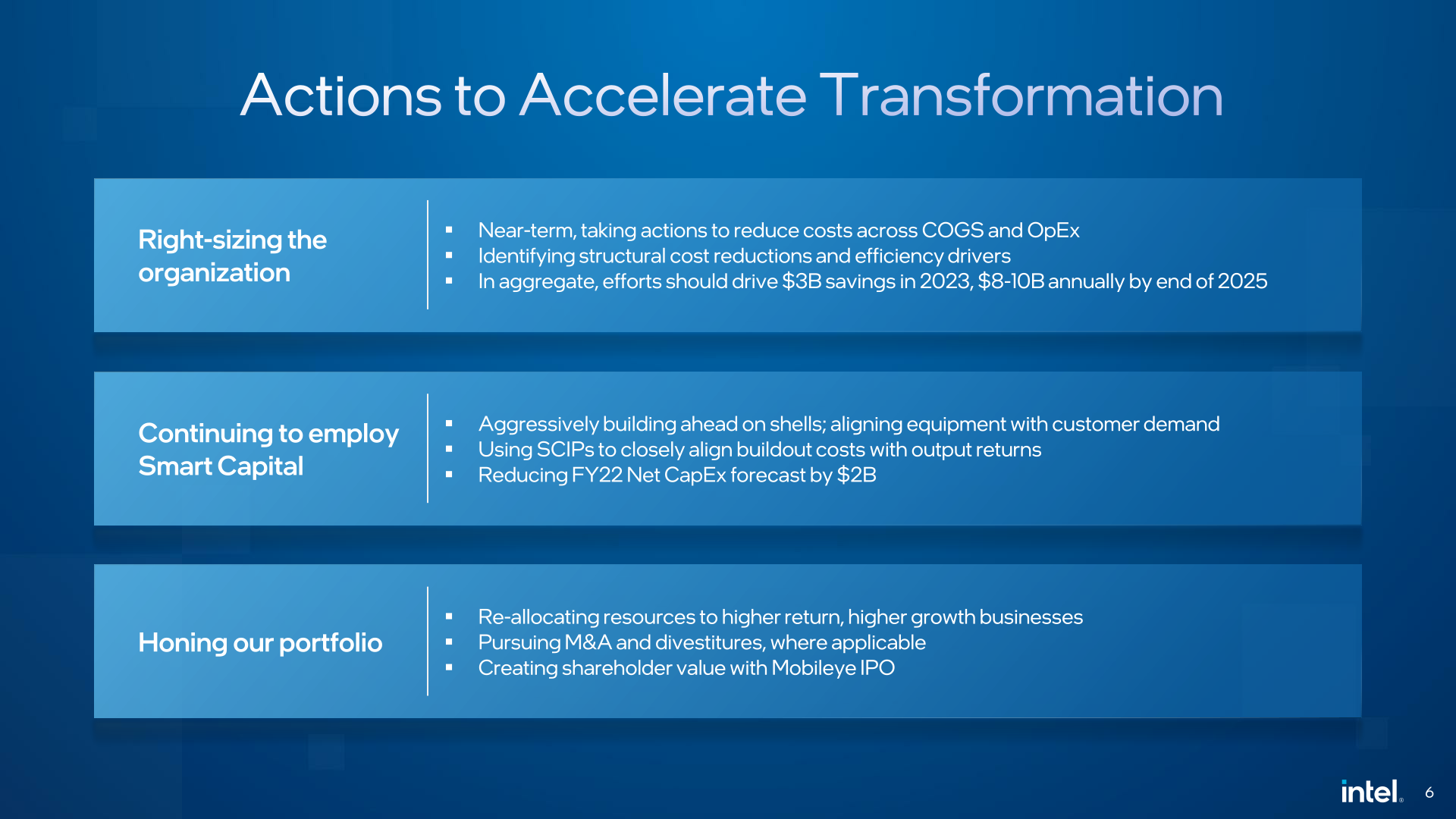

Given that Intel’s revenue and profitability aren’t expected to recover soon, the company has made clear that cost-cutting is underway, including job cuts. No specific layoffs have been announced yet (some of these will undoubtedly be announced soon, as the earnings period is over), but to implement the imminent layoffs, Intel is known to have paid $664 million in restructuring charges in the quarter. At current headcount, Intel has approximately 114,000 employees.

Overall, Intel wants to save $3 billion in costs by 2023, and it’s accelerating toward 2025. And since capex is one of Intel’s biggest costs, this is also where they make the bigger cuts. The company said it plans to continue manufacturing fabshells and add equipment as demand grows. This alone should allow the company to cut his 2023 capital spending by $2 billion.

Finally, as Intel seeks to focus on high-margin businesses, it also leaves the door open for mergers, acquisitions, or divestments that benefit the company. We don’t have anything specific to announce here today, but like other companies tightening their belts, Intel plans to explore all options.

Overall, Q3 2022 didn’t hit Intel in the same kind of way that Q2 did, but the message from the company is that the challenge isn’t over yet. As his CEO Pat Gelsinger said in the company’s earnings call, “We are aggressively addressing costs and driving efficiency across the business.” Intel is working on a restructuring to survive the rest of the recession cycle.

{kind=link}