Liquidations expected as Bitcoin open interest, leverage ratio spike higher

Over the past month, Bitcoin has traded relatively flat between $18,400 and $22,800.

Against the deteriorating macroeconomic backdrop and the escalation of events in Eastern Europe, some analysts see this as the beginning of BTC decoupling from legacy markets.

There is no shortage of bullish calls in the short term, but what are the indicators for on-chain derivatives suggesting?

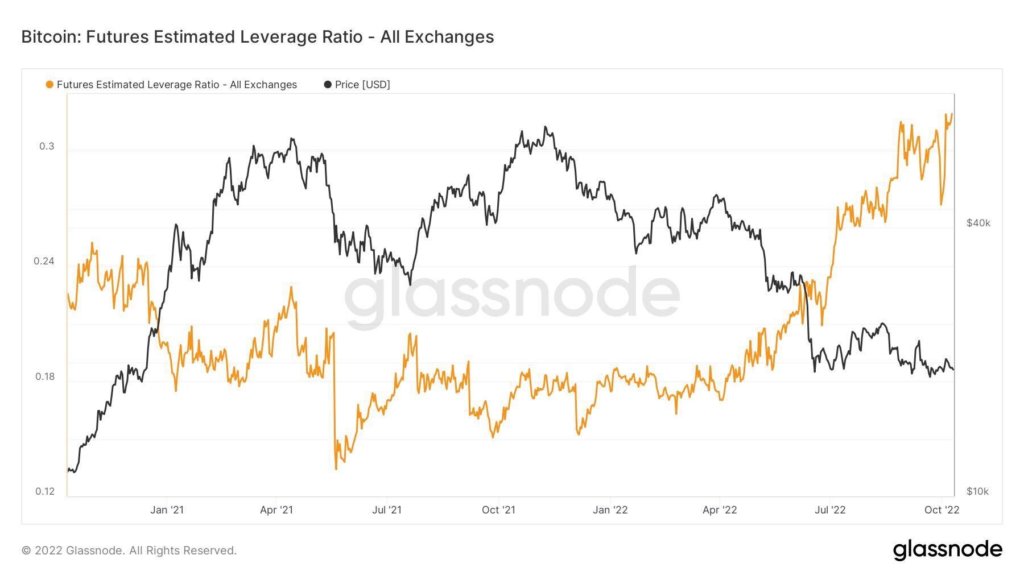

Bitcoin Futures Estimated Leverage Ratio

The Estimated Leverage Ratio (ELR) metric for Bitcoin futures is the percentage of open interest divided by the exchange’s reserves. Open interest relates to the number of derivative contracts open (unsettled) at a particular point in time.

This indicator represents the average leverage currently used by derivatives traders in the market.a A high ELR often coincides with BTC spot volatility. In this scenario, derivatives traders are exposed to the risk of liquidation.

The chart below shows a record ELR of 0.34, suggesting high liquidation risk. While we can’t give a definite direction, a downward move is more likely given that BTC is trading on a higher macro timeframe.

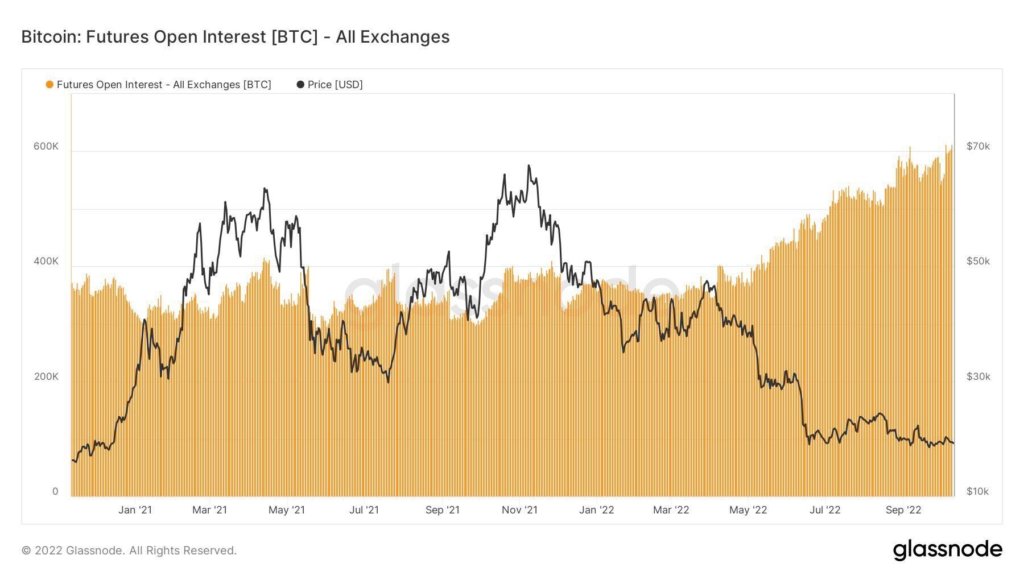

futures open interest

As mentioned earlier, open interest is a measure of outstanding futures contracts in a given time period. High open interest means new traders are opening positions, resulting in net gains.

The chart below shows the gradual rise in open interest from its annual low in March to now. With around 600,000 contracts currently read, it’s clear that derivatives traders are piling up despite the deteriorating macro environment.

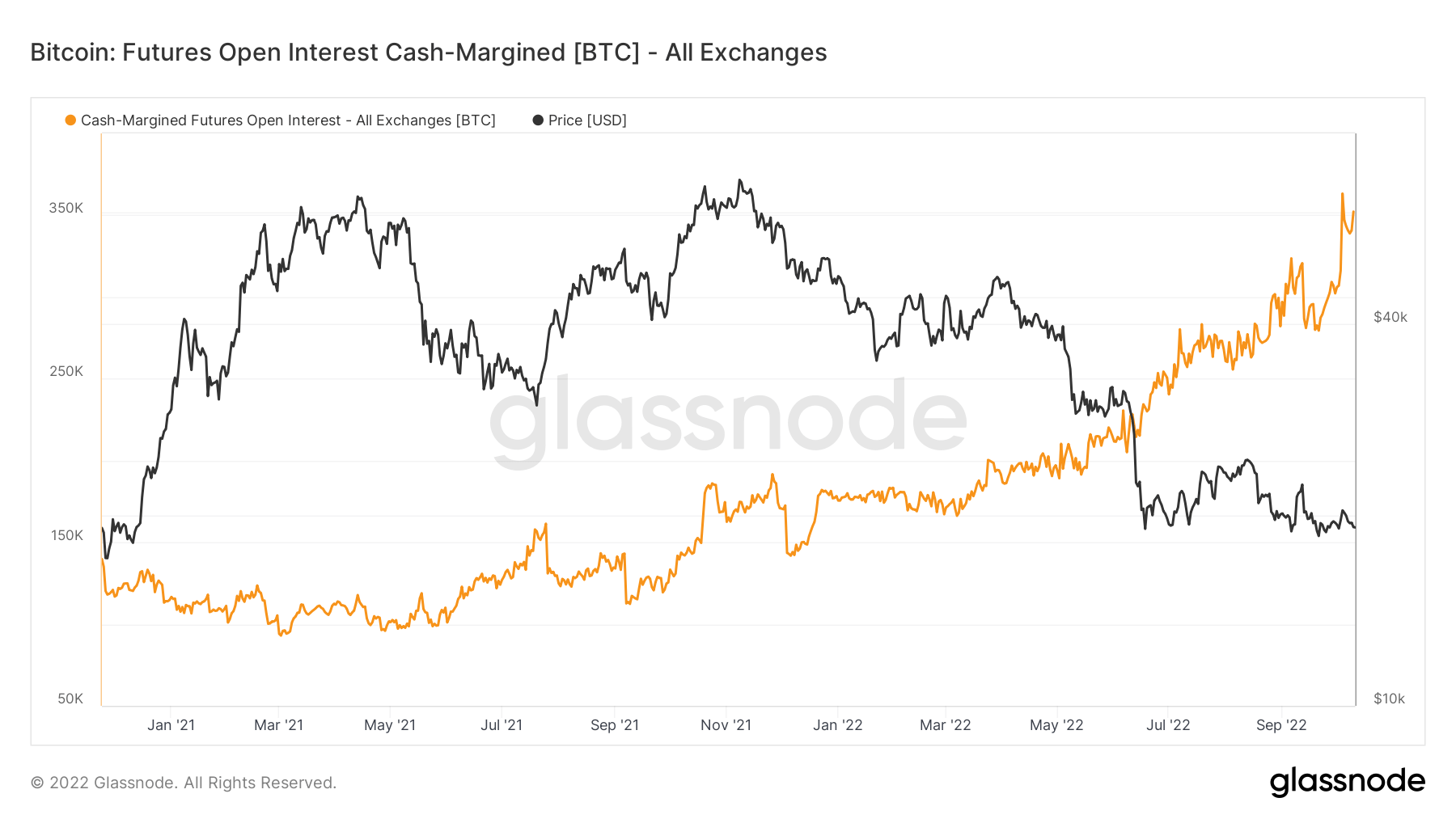

Similarly, Open Interest Cash-Margined (OICM) also represents interest, but from a money flow perspective. As expected, Bitcoin futures inflows are trending upward as open interest has surged since the lull in March.

Aside from the mid-September decline, OICM resumed its uptrend, peaking at around 360,000.

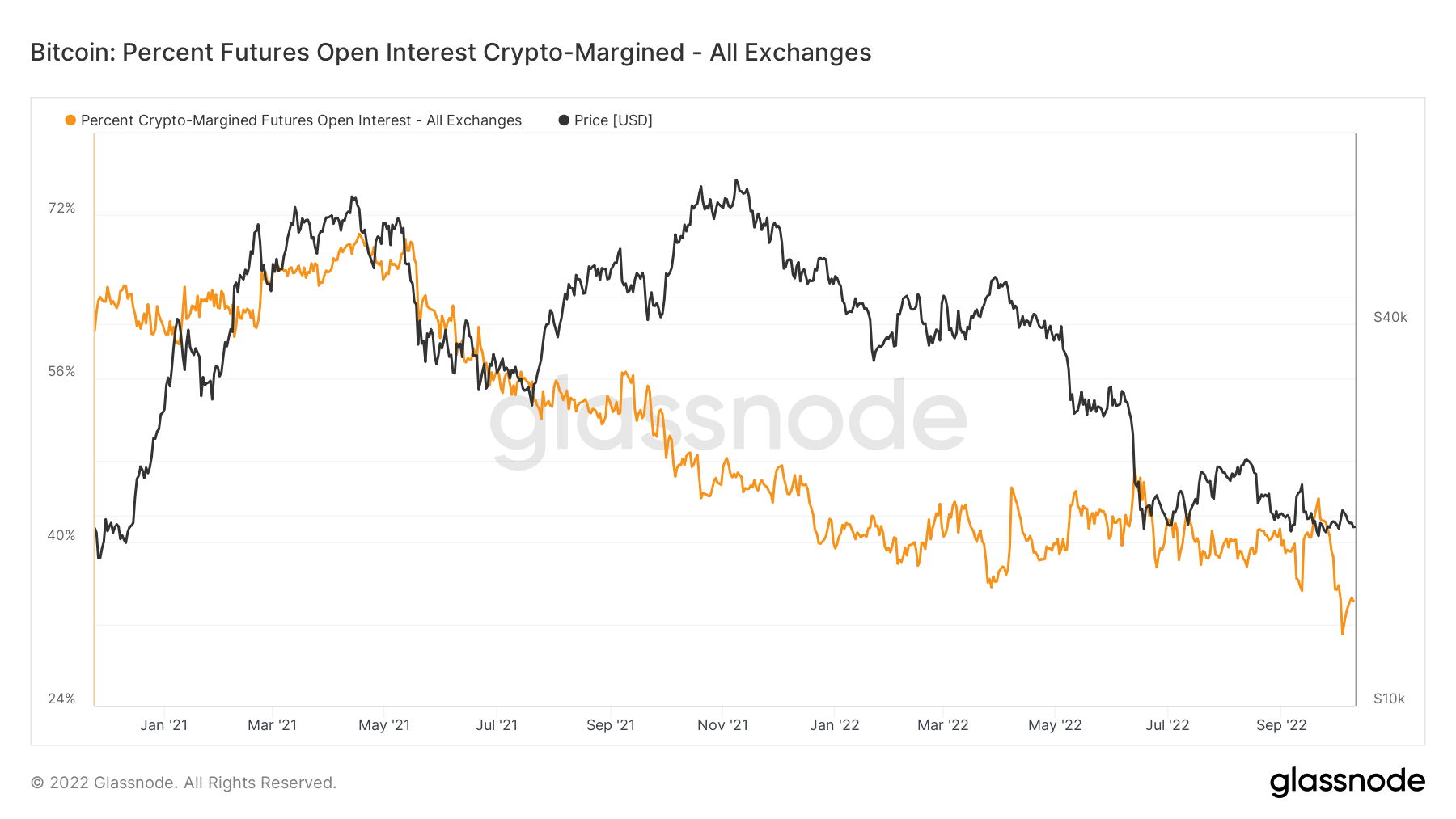

During the 2021 bull market, the majority of traders were using Bitcoin to initiate futures contracts, presenting significant but acceptable risk during the euphoric period.

Currently, in a bear market, traders are switching to cash, and as a result, the Open Interest Crypto Margin Index has fallen from its April 2021 peak of 70% to its current 38%.

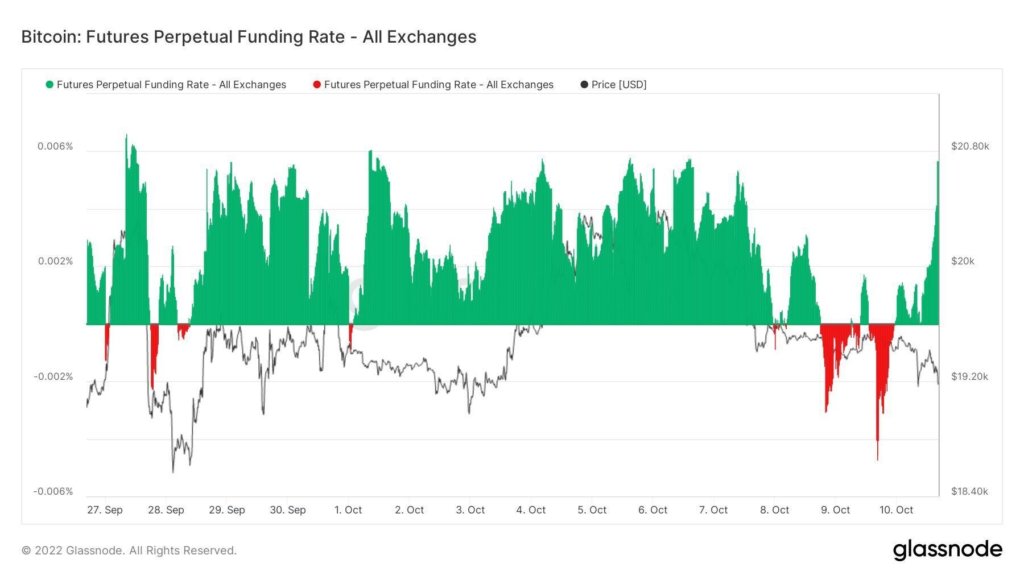

Futures Perpetual Funding Rate

Futures Perpetual Funding Rate (FPFR) refers to periodic payments made to or by derivatives traders, both long and short, based on the difference between the perpetual contract market and the spot price.

During periods when the funding rate is positive, the perpetual contract price is higher than the mark price. Therefore, long traders pay for short positions. In contrast, a negative funding rate indicates that the price of the perpetual contract is lower than the marked price, short his trader pays for the long.

This mechanism is designed to match the futures contract price with the spot price. FPFR can be used to measure trader sentiment. That is, willingness to pay a positive interest rate suggests a bullish belief and vice versa.

Funding rates have been nearly neutral since May. Since late September, however, the chart below shows that the funding rate has been mostly positive, recently flipping between negative and positive funding.

Over the weekend ending October 9, the discovery rate plummeted to -0.005% before making a big move in the opposite direction, reaching +0.0058%.

With estimated leverage ratios and open interest at all-time highs and positive funding rates predominating, the cryptocurrency market is extremely hot and over-leveraged.

A widespread liquidation could occur in the near future, triggering a Bitcoin-led asset price decline.